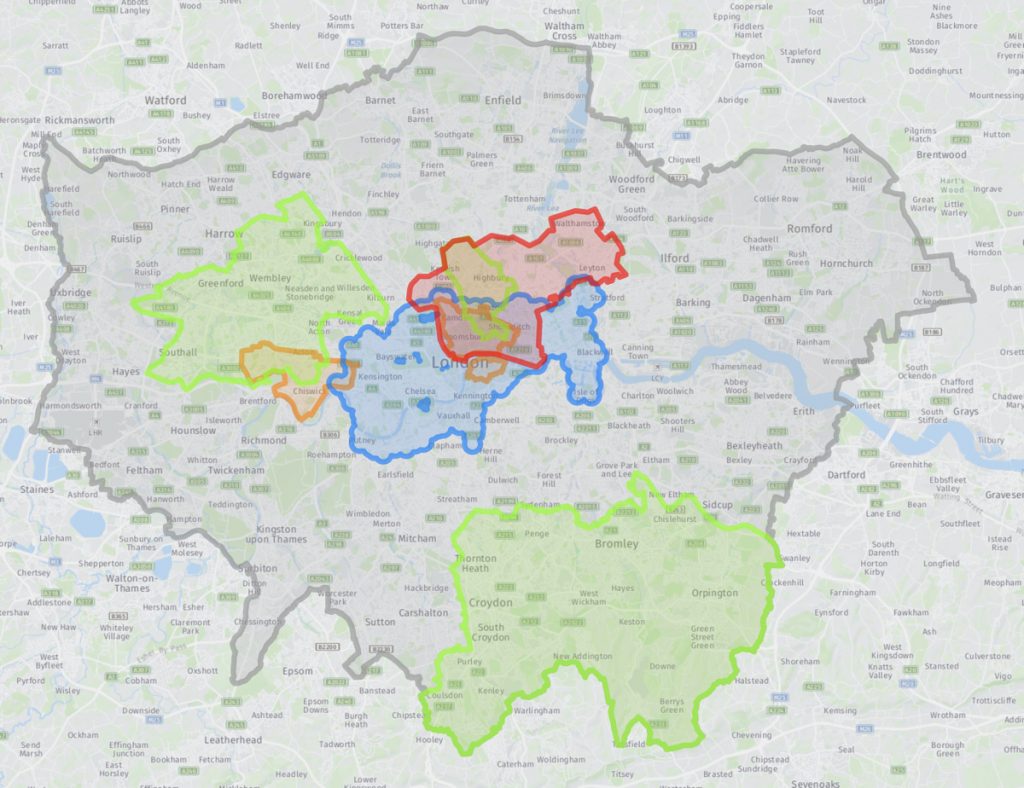

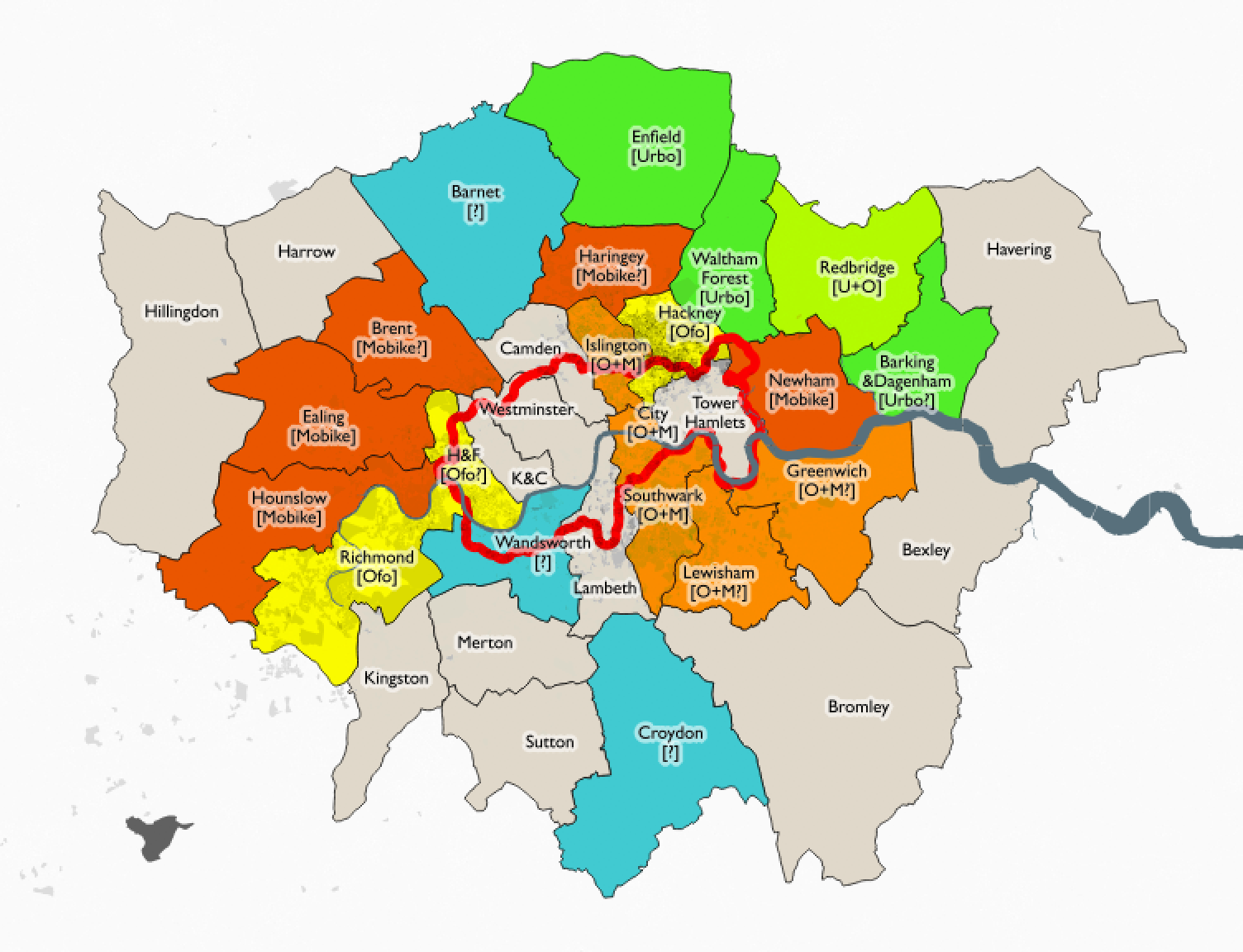

While TfL ponders London-wide regulation and freezes Santander Cycles, borough-by-borough rollout (and sometimes rollback) of dockless in London continues. I’ve rated each borough based on its provision – current, announced and rumoured (so likely some errors) of this all-important last-mile mobility addition to our streets:

Key

- A – 2+ operators in/confirmed, at least 1 of which covers/allows >75% of borough and the other covers/allows >25% of borough

- B – At least one operator, in/confirmed, covering significant part (>25%) of borough.

- C – Operator(s) only covering small area, and/or only rumours of new operator.

- D – No operators or positive news.

- + – Improvement expected soon.

- * – Simple projected % for 2018, based on Census data – 2011% and 2001-2011 rates of change

I intend to keep this table up to date as things change, and make corrections where I discover things are wrong above. In case it doesn’t view correctly for you, you can see the full table on Google Sheets here. You can also see operator open data scores – check the tab at the bottom of the sheet. Nobody gets an A on this measure, though (GBFS+journeys).

Current (May 2019):

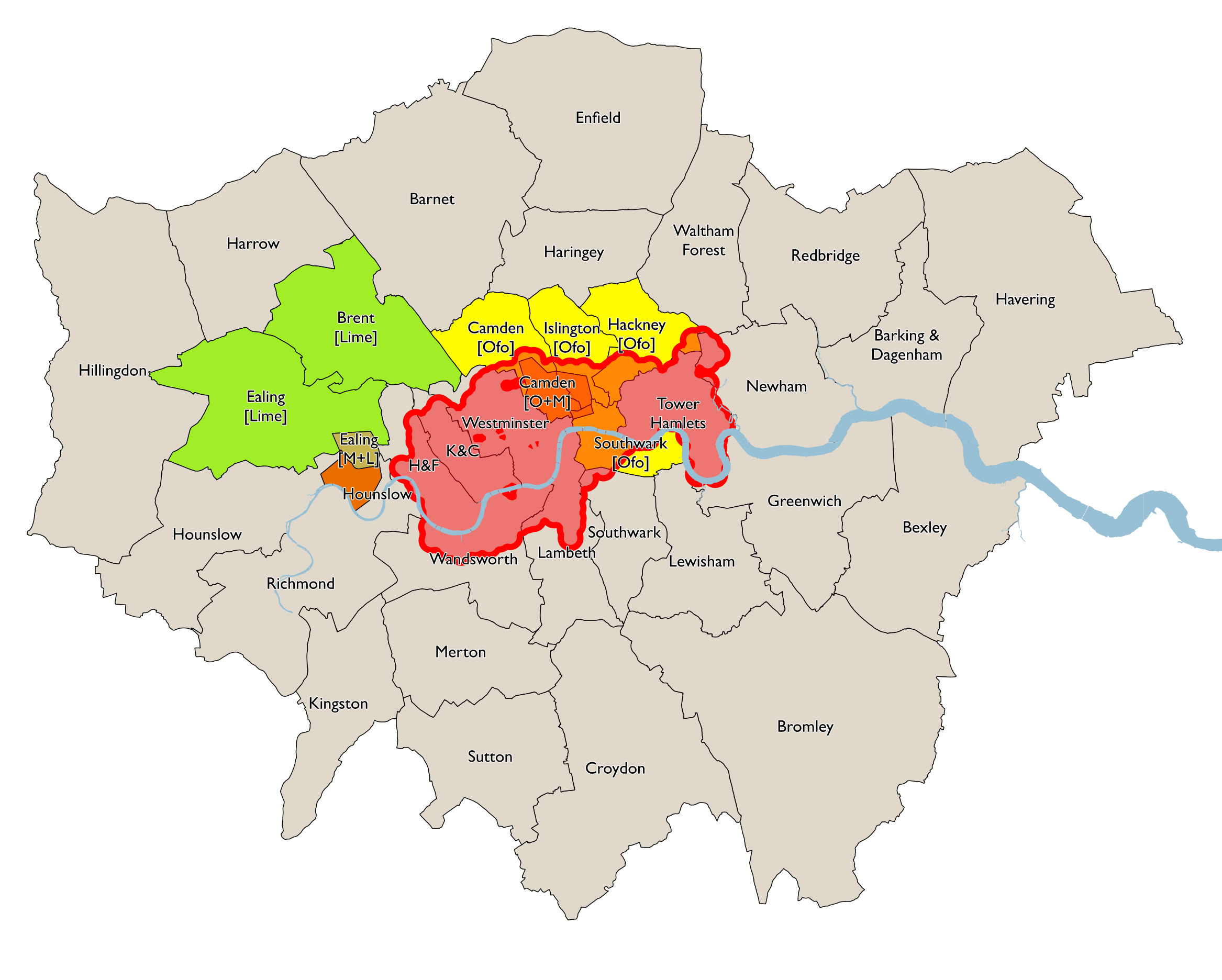

Previous (January 2019):

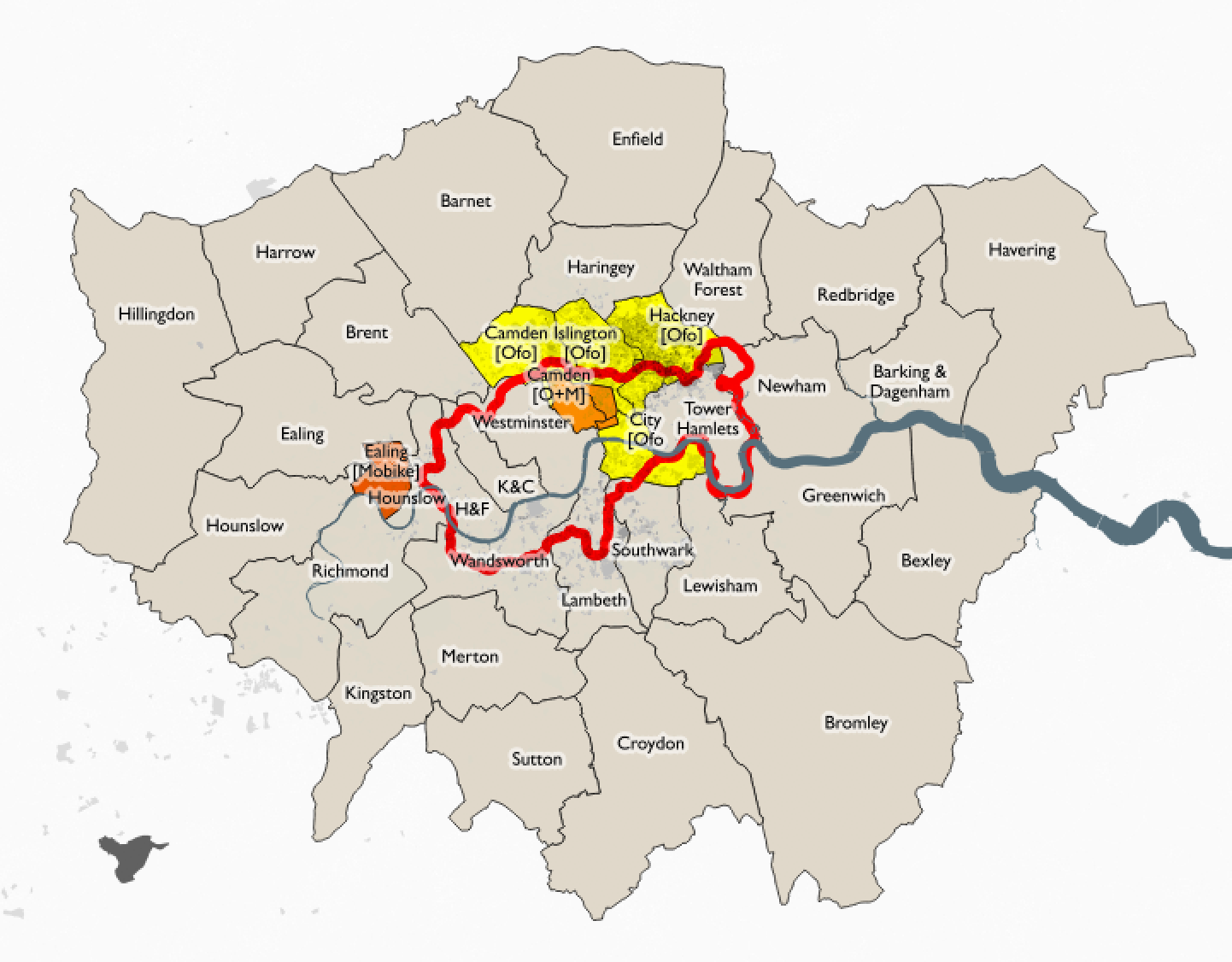

Previous (October 2018):

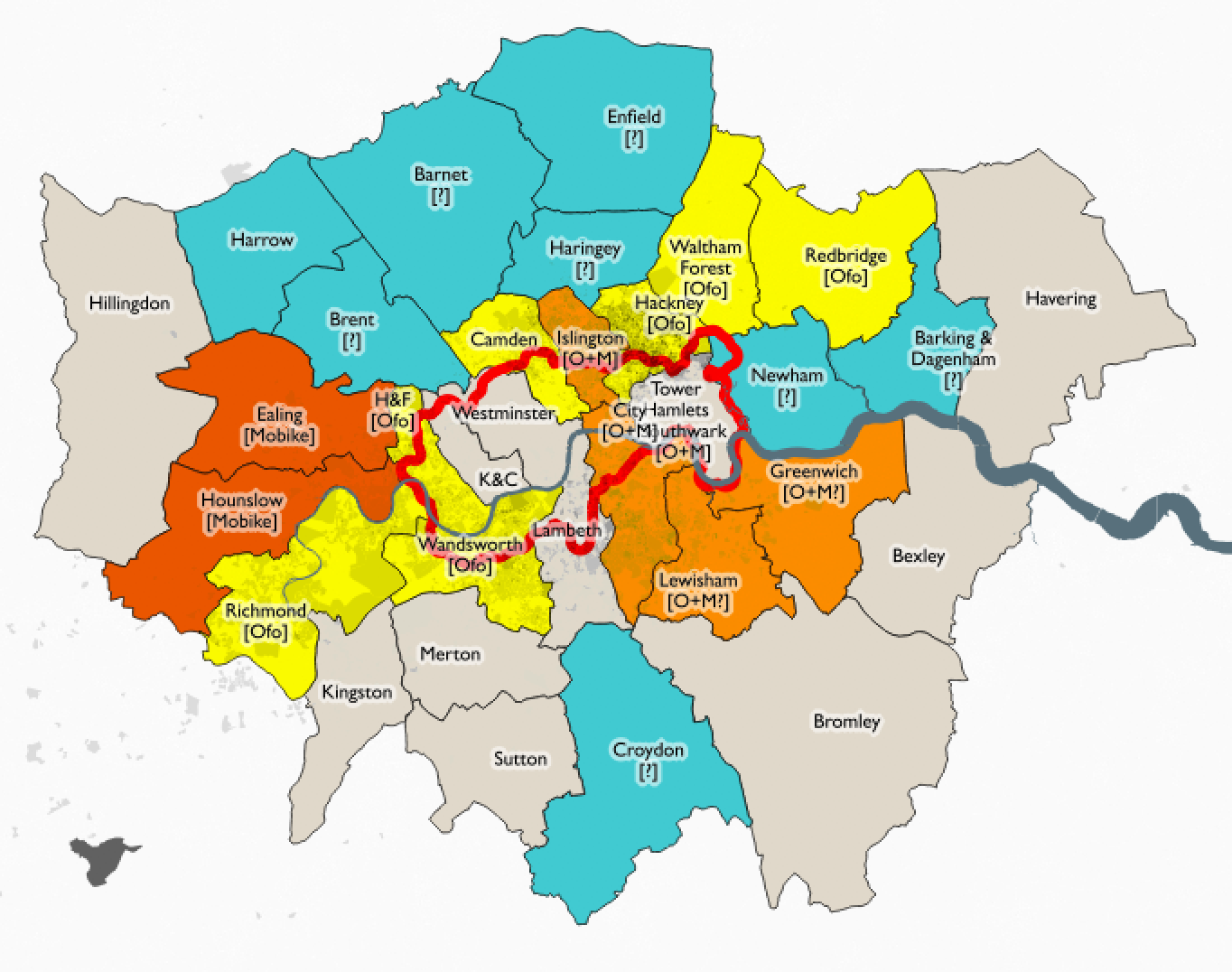

Previous (June 2018):

Previous (May 2018):

See also my thoughts on the future of bikeshare in London in general.

3 replies on “Bikeshare in London – Borough Update”

Useful that you are monitoring and listing. It is also interesting to note the different tariffs and tariff caps that are offered, and the fact that most ‘dockless’ hire systems are still required to have bikes hired and returned to defined locations.

This detail was rapidly learned by DB Call-a-Bike, possibly the first automated dockless bike system in Europe …. in 2001 (ignore the hype from Chinese operators!). A typical docked bikes system requires around 50% more docking points than bikes in circulation, and the short hire charging tariffs generally need to deliver 8-16 hires/bike/day in a sustainable, and well utilised system. Clearly more than 16 hires/day will see people waiting at hire hubs/docking points to grab a bike as soon as it is returned. Early ‘closed’ systems also determined that 20 ‘active members’ per bike began to adversely impact the levels of service.

London got its first automated public bike hire in 2004 when OYBike launched in West London – they closed in 2009 when it was clear that a TfL (& Serco/Barclays) – backed scheme would push them off the streets. They had not prequalified to bid (due I gather to lack of financial ‘weight’ – despite selling a 49% share to Veolia Transportation). 6 bidders prequalified, but the conditions set saw JC Decaux not even bidding, and Call-a-Bike dropping out, leaving the final pair as Clear Channel (operating public bike hire since 1997) and a Serco-Bixi amalgamation of 2 other bidders (Serco with resources, Bixi with a new system due to have first operations in Montreal in 2011).

The caveats and requirement for built in docking stations were onerous – the hugely successful roll-out of the same Bixi bikes in New York used the bolt-down modular docking station units, which can usually be installed in 24 hours with solar panel power, and wireless data links (and not the long lead times for a TfL-spec ‘special’).

Note that Donkey Republic (with a slightly different operating tariff) claim a London operation is in place, with bikes at 7 Network Rail managed stations – no signage and from what I can find out no agreement with Network Rail to use their bike parking racks.

Abellio also has Bike&Go at Liverpool Street, but the system currently is far from seamless or 24/7.

Brompton Hire has several docks around the GLA area, and delivers for a specific market – hires are typically for a working week or a block of several 24 hour periods. Typically the London units are operating at over 70% of capacity (6 bikes hired out at any instant for an 8-bike unit), and with the daily hire regime and pre-booking of hires/return slots, a unit can run at over 100% capacity (more than 1 bike on hire for every locker). Developers and large corporate offices have installed/are installing units around London – some private (HSBC) and some public (Kings Cross/Bishopsgate) for staff/tenants/public use. Brompton Hire has been running in London since 2009.

Outside London Serco has now won the concession for Edinburgh, with an improved version of the Pashley bike now replacing the Bixi original bikes, which at 7 years old are reaching the end of the flat-line part of the bath tub curve (Royal Mail replaced their bikes at 7 years) and Nextbike (set up in 2004) has been delivering in Glasgow, Cardiff, Bath, Milton Keynes, Stirling, Birmingham (to come) with Universities at Warwick, Swansea, Brunel, Portsmouth, with the home-grown Hourbike in Oxford, Reading, Liverpool, Nottingham & other locations, plus other beach-heads I’m aware of for incoming operators in Slough and Falkirk.

There is a wide spectrum of contractual relationships, tendering processes, tariffs and funding models as this nascent public mobility offering develops, with some schemes more sustainable than others, and some ‘contracts’ secured by offers based on optimistically forecast revenues. Of all the systems perhaps Nextbike currently offers the widest palette of choices and tested operating models – formal docks & pillars, through to dockless, and hire access through phone app, Q/R code, SMS release code, call centre, RFID card. The option of selling the bike branding delivers a base-line revenue, and the electronic back office enables individual, or corporate rates to be used across a city fleet. Note also that once a member or signed up to a world-wide scheme, you basically can use those bikes anywhere in the world, and in London Ofo confirms that inter borough trips can be made.

[…] See also my London borough bikeshare scorecard. […]

Great summary and overview of current position. Thanks Alastair Majury