The Guardian newspaper has published an online article about the rise and fall of dockless bikeshare, focusing on the pure dockless systems in England (there aren’t any in the rest of the UK) that grew in 2017, and then shrank last autumn. The article extensively used some of the geospatial boundary data that I have – you can can see this on Bike Share Map. It also used some estimated counts and also looked ahead.

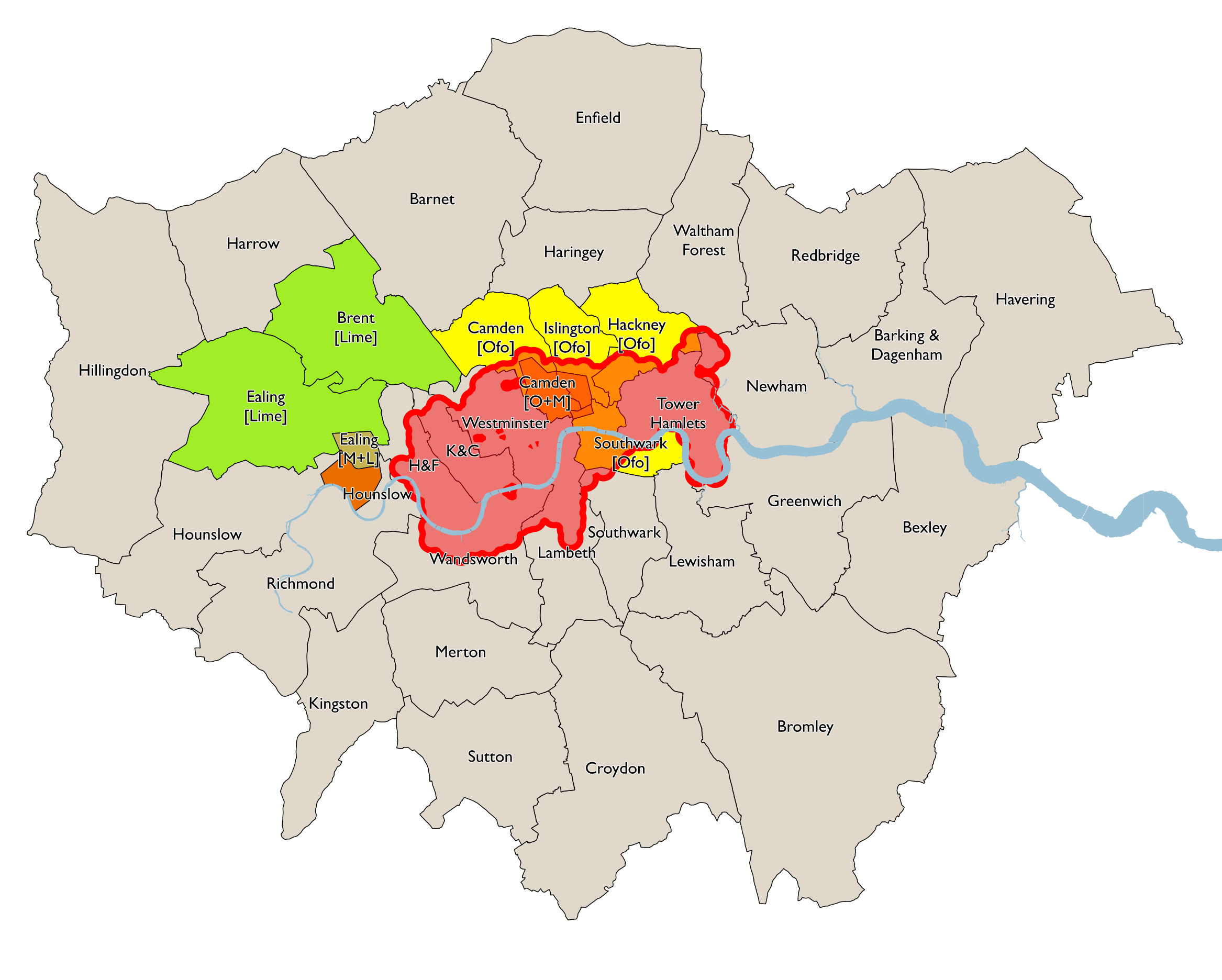

Meanwhile, there are various clues as to the next wave of dockless bikeshare, here in London. It looks like there are going to be at least five, possibly six players this year that will be complementing and/or competing with the incumbent Santander Cycles system that still has more bikes on the streets (10000) than all the pretenders put together:

Mobike, after their summer expansion and autumn radical contraction, appear to have got things under control and have started expanding again. They remain operating in two main areas – in west London (around Ealing, Acton & Chiswick) where they are not competing with Santander Cycles, and in central London (Camden Town, Bloomsbury, Angel, Bankside and the City of London) where they do. They are keeping their operating areas small, and their densities high, and are staying out of the inner city London areas where they will have had great numbers of their bikes stolen and vandalised. This is an eminently sensible business decision even if it restricts the usefulness of the system in a broader London context. Their fleet is largely upgraded to the Lite model which is much more comfortable to ride. No sign of any pedelec (electric assist) yet. They still have a very high out-of-zone charge, which coupled with their often changing operating boundaries means that users need to do some research before hiring, to avoid unexpected penalties. This lessens the scan-and-go readiness of the systems. There are around 1800 in the fleet currently.

Lime‘s pedelec system was looking good, with a carefully run system with no penalties for starting/finishing out-of-zone (as long as you don’t go out of London itself). Although I found the actual cycling experience not amazing, I am probably not the target market, and right now it is making a positive contribution to London’s Mobility as a Service (MaaS) options. However… Lime in the US have had a change of policy recently, switching all their pedelecs to escootershare. This doesn’t bode well for London in the long term, as the large MaaS companies are all about economy of scale. Maybe London will be quickly and genuinely profitable for them, and they’ll keep running the system here. We shall see. They currently have around 1400 bikes in their fleet in London.

Beryl’s Secret Cycles pedelecs remain in active pre-launch development. They are being developed right here in London and the group are taking time to get it right. The odd Secret Cycle is occasionally seen on the streets of London, and a council test is taking place in Enfield. It looks like they will, after launching in Bournemouth, be bringing their system to Islington, Hackney, Tower Hamlets, and presumably also Enfield. There are currently around 10 in their fleet, none for public use.

Freebike pedelecs are currently being tested by Waltham Forest council employees, so it may be launching there at some point soon. However, a City of London decision suggests they may also be coming to the heart of the capital too. This is a small place so having all the various operators in here could be interesting. However, half a million people do commute into the so-called Square Mile every working day, so there is always going to be a big focus here. There are currently around 10 in their fleet, none for public use.

JUMP pedelecs are also likely coming. Their parent, Uber, had a job posting out for a London-based operations/field manager. With Lime’s US pedelec retreat, JUMP are the sole US-based pedelec system and are increasingly finding they are the only bidders for US city dockless systems. London’s competition will be harder, thanks in no small part to escootershare remaining illegal here. JUMP will likely go big when they launch. They will also be able to leverage their huge existing base of London Uber users – no separate app needed!

Finally, and this is pure speculation on my part, but YoBike runs some reasonably successful systems in Bristol and Southampton. The platform that YoBike is part of is SharingOS, and they are based in London. I am sure they would to have a physical system a little closer to their base.

If there are going to be 5+ systems in central London, then the authorities are really going to have to get their act together re managing parking for these fleets. A mass expansion of cycle parking hoops, or taping rectangles on pavements for them, is going to be needed.

A Beryl Secret Cycle on test, spotted in the City of London. Photo courtesy of Angus Hewlett.

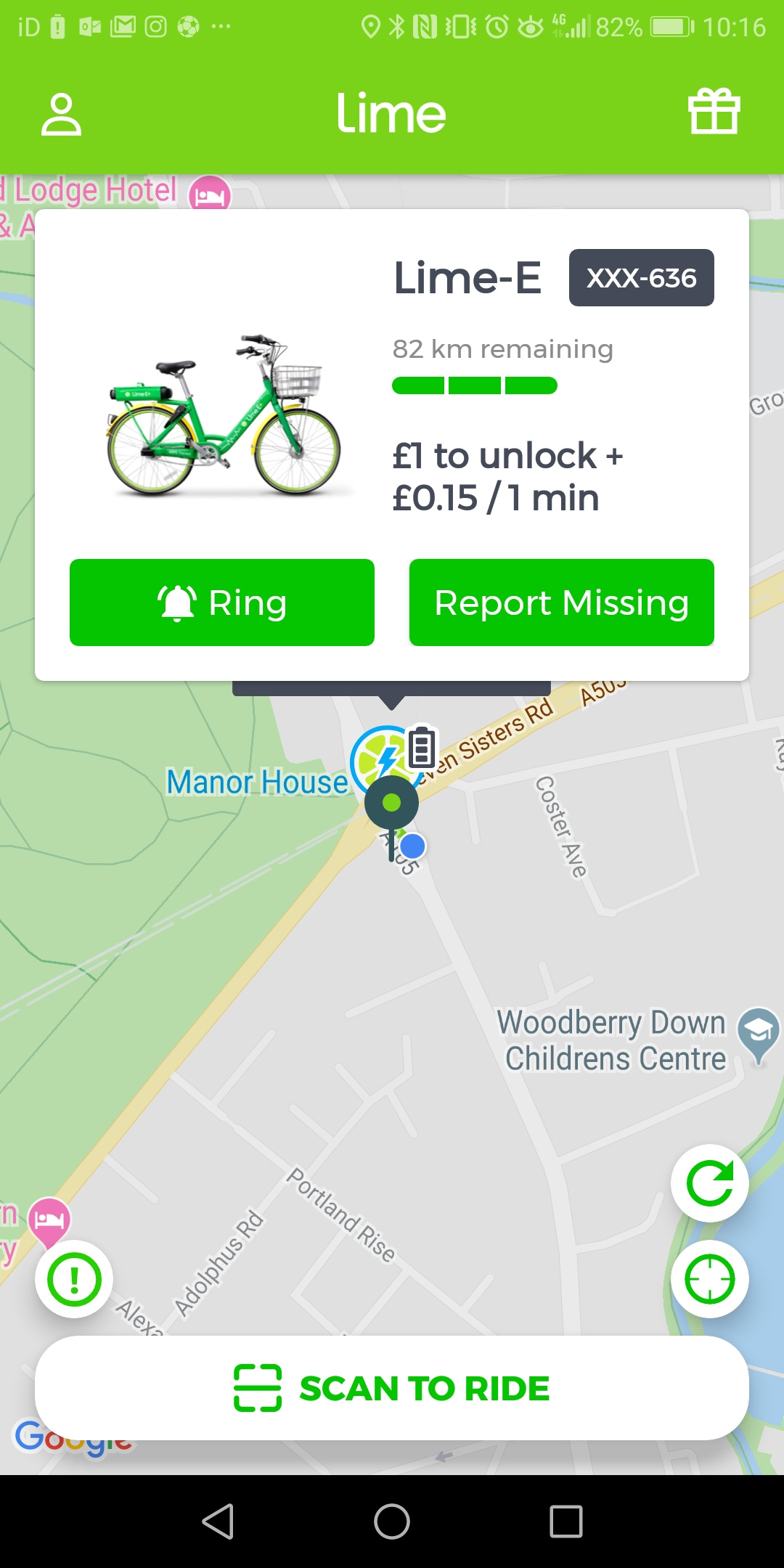

A puncture on my own bicycle on my way in to work this morning found me grinding to a halt outside Manor House station – not the worst place to have a flat tyre, as the tube from there will take me into work in around 20 minutes with just one change, for £2.40. (The other option was a single bus for £1.50, taking 30 minutes – although easily longer if it gets snarled up in traffic). But as I dropped my bike off in the bike stands beside the entrance, I noticed another bike – a chunky, green-and-yellow coloured beast. It was a Lime-E bike – London’s only (so far – others coming) electric bikeshare, also parked beside (but not chained to) a stand:

Surprise mobility option, sitting at a bike stand in North-East London.

It was well out of zone but Lime (currently) allows hires starting and finishing out of zone – a pragmatic decision presumably based on the lack of cross-borough policy, the bikes being relatively well managed by the operator, and there not being too many of them cluttering up and causing non-user complaints:

Plenty of out-of-zone Limes available…

I hadn’t tried Lime so far, although it launched last December – I was put off by the £1/hire+15p/minute cost – that adds up quickly. But, I needed to get to work and it was right there. Surely this bike could prove to be an effective alternative mode of transport, for my immediate commute requirement?

I already had the app installed on my Huawei smartphone, but had not put in payment details – only when trying to scan did it prompt for a payment card. Android Pay stepped in to automatically add my credit card details, however Lime didn’t like the two-digit year supplied by Android, requiring a reenter of that section.

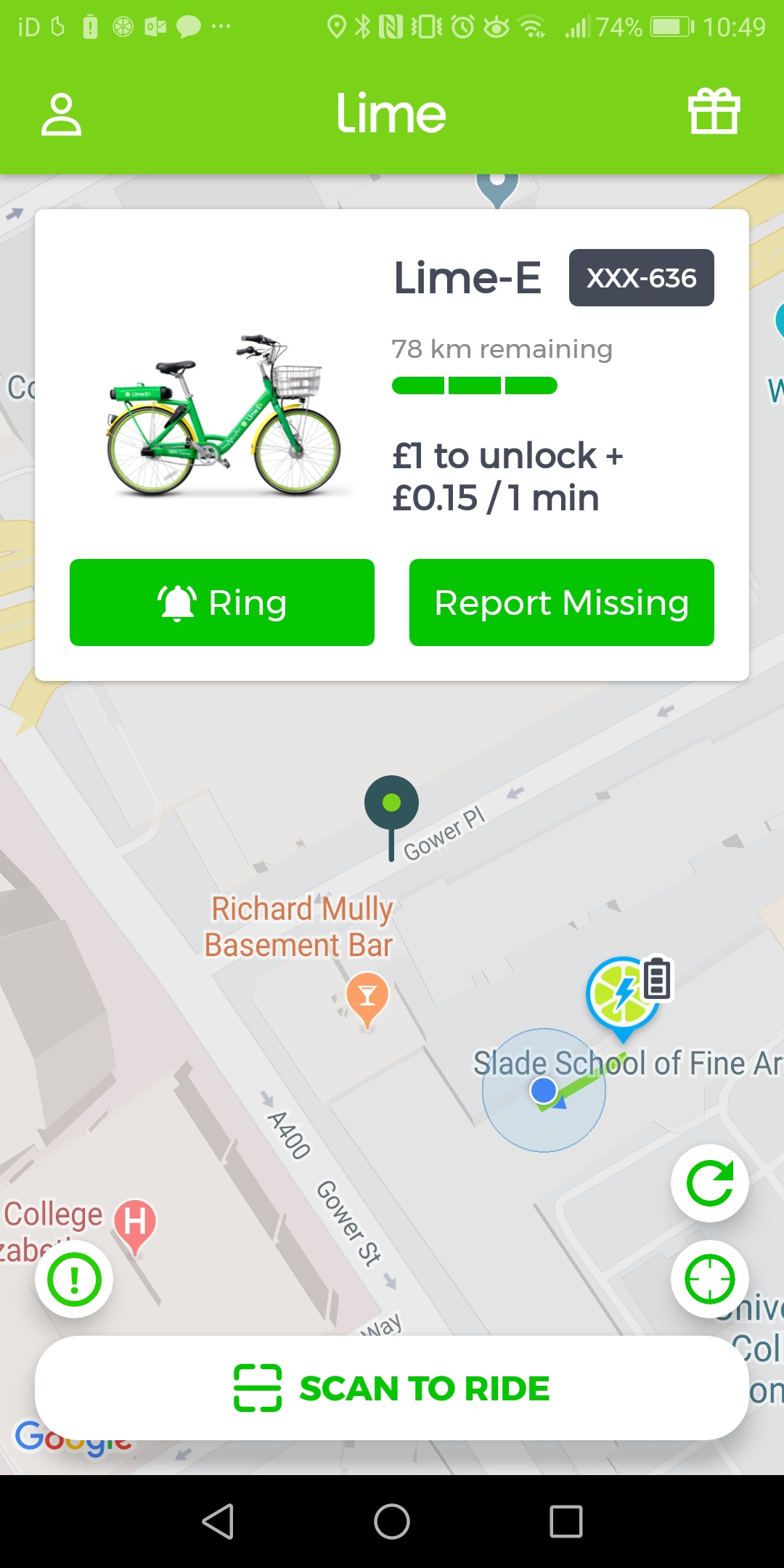

The app confirmed that this was a hireable bike and that it had a decent amount of charge on it – 86km! I could almost get to Oxford with that:

My ride. Looks good on the app and in real life.

Then, a rescan and the bike unlocked with a click in a couple of seconds. (Interestingly, the wheel-lock was quite a small one, not the chunky ones that appear on Mobikes now to try and stop rampant theft of them.) Something (the bike, battery or the app – not sure!) played a jolly tune to indicated success, and I was off. Unfortunately I quickly noticed the bike loudly jolted with each wheel turn – possibly a buckled spoke or other problem with the wheel – it was not enough for me to abandon the journey, but was not something I would leave before fixing. Later on, something else made a plastic rattling noise at the back of the bike every time I pedalled. Maintenance (or lack of it) was a problem with the non-electric dockless bikeshares in London. I was hoping that the more expensive electric bikes would have a more rigorous repair regime. Maybe they do and I was just unlucky.

The initial acceleration boost given by the battery was great – straight across the lights and down to Finsbury Park. However, almost immediately it just felt like a regular bike – there was still a boost at faster speeds, but it felt like it was just countering the heavy battery, rather than genuinely making it easier than a regular bike. I didn’t feel slower than my regular bike – but it didn’t feel like it was any less effort either. There is only one gear, so the only thing you can do other than pedal, is to ring the handlebar bell. The gearing is OK – it’s certainly better than the Mobike/Ofo/Urbo ultra-cautious setting.

I was keen to measure the “configuration” for the electric-assist, so stopped after around 3km, at the bottom of the main remaining uphill on the route – up Camden Road past the old Holloway Prison – to attach my Beeline smart compass – not for its primary navigation purpose, but to get an idea of the speed I was travelling at. The speedometer function has rather nice analogue-style needle, and was a useful way to see my speed without looking at my phone, even if it is based on my phone’s GPS and therefore lags by a few seconds.

Beeline smart compass on a Lime bike – testing the electric assist at different speeds.

It was undoubtably nice to accelerate up the hill with the battery doing the initial work. It seems that, between 0km/h and around 12km/h, the battery does most of the work. From around 12km/h to 20km/h (my normal peddling speed) it gives a slight assist – not really noticeable but presumably useful for longer journeys. From 20km/h to the legal maximum 25km/h I’m not convinced the battery was helping at all – or if it was, it was just partly countering the weight. It was hard to pedal the bike above 25km/h even downhill on a clear road – but that’s presumably by design – bikeshare is generally meant for quieter roads and less experienced users, where a slower speed is safer, rather than me trying to match the vehicular traffic on a sometimes busy “red route” major road.

However, it would be nice to have a much bigger boost between 12km/h and 20km/h, so that you only have to be doing significant peddling work at the top of the range. I feel more tired out than I would have on my own normal pretty cheap road bike. It took me 22 minutes to get in – exactly the same amount of time as my own bike would have. Average speed 19km/h according to my smartwatch – pretty standard for me. Certainly my fastest journey on a bikeshare bike in London.

Journey’s end, at the Santander Cycles rack near UCL. Note also the Mobike.

I parked my bike alongside a Santander Cycles rack. There was also a Mobike there. I really like the idea of dockless cycling bikes being available at the “empty” ends of Santander Cycles docking stations – it seems an “obvious” place to leave them, it’s also a good place to “advertise” to people who are in need of a bikeshare of some sorts. (Incidentally, the poster in the Lime basket refers parking in the “sidewalk” twice – needs some UK localisation here, we call them pavements!)

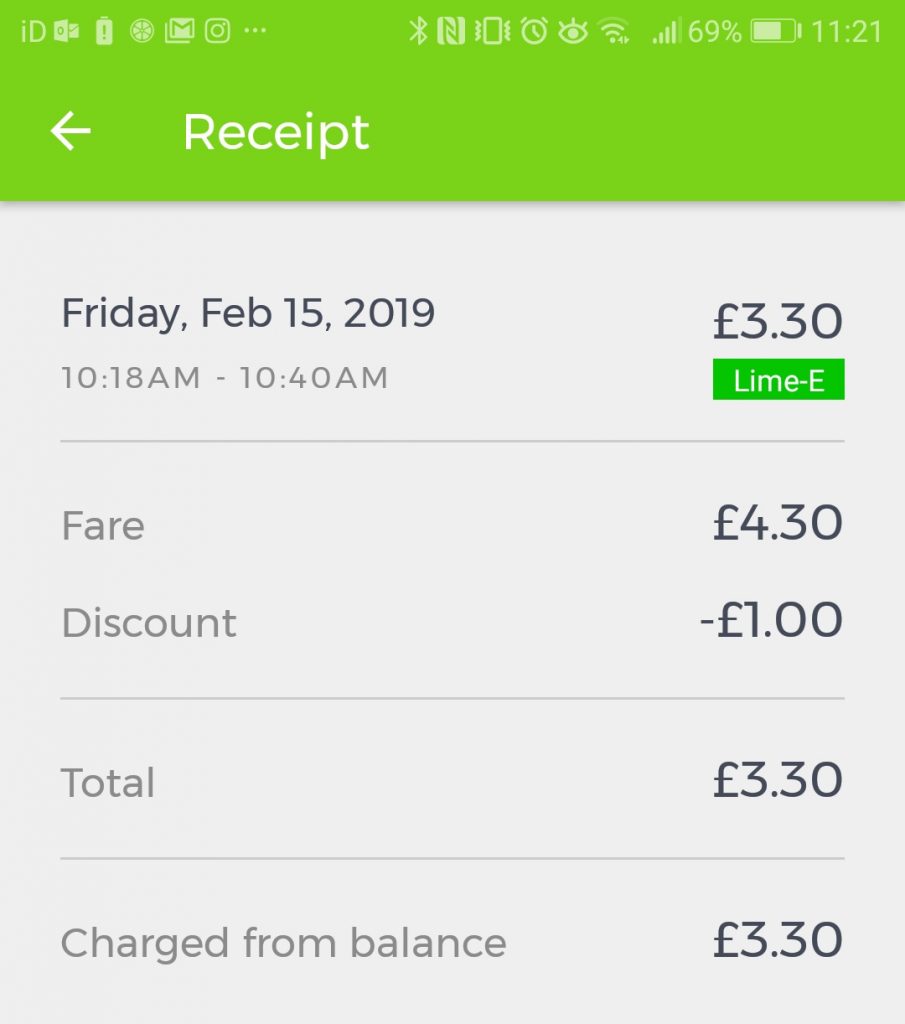

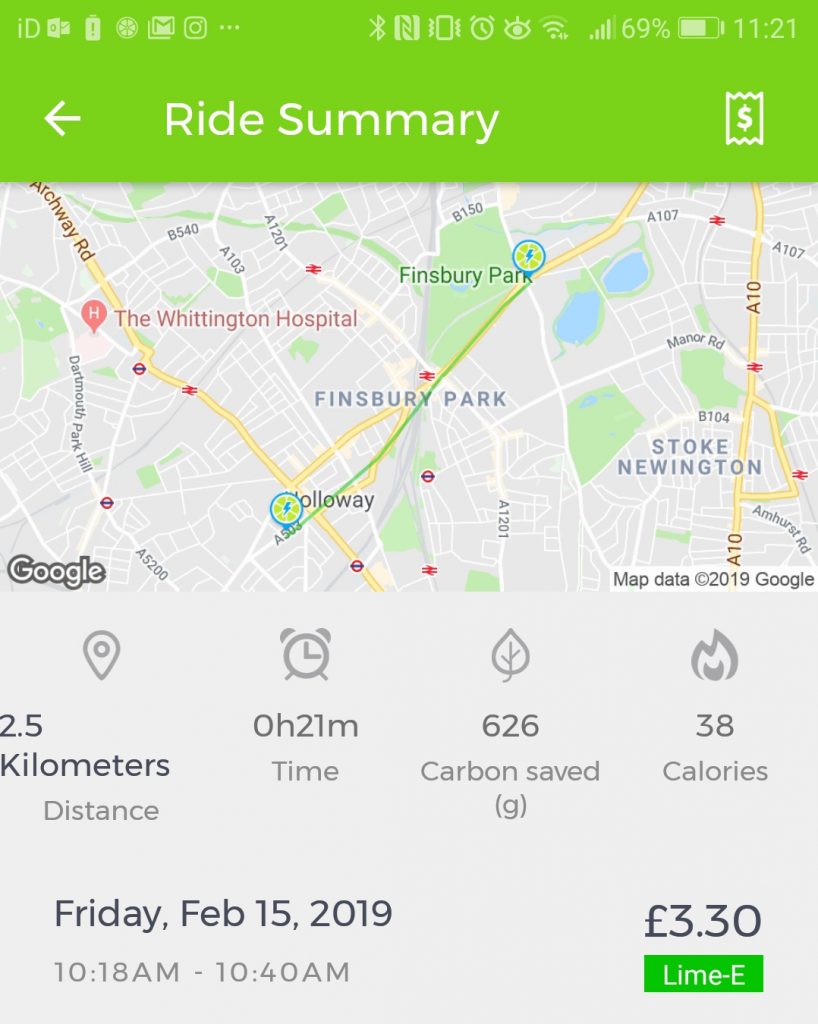

My fare. This is expensive for a Zone 2-1 journey in London.

A bit of bill shock though – £4.30, as it was a 22 minute journey (£1 hire + 15p/minute for 22 minutes.) The £1 was, at least, waived as this was my first ride and I was on a referral (btw use my referral code RVDG4MS if you want your own). The pricing structure means that the temptation to (safely) jump red lights was strong – much more so than on my own bike. There are a lot of traffic lights on the route and everytime I hit red on one of the bigger junctions, it will have cost me 15 pence. That’s, unfortunately, a pretty powerful financial incentive to break the law. I didn’t (obvs) – but I can sympathise somewhat with the Uber Eats and Deliveroo cyclists who are numerous in London but aren’t the greatest at obeying the rules… for them, like the many delivery vans in central London getting tickets for illegal parking, the speed/penalty balance is tilted towards bad behaviour.

Also, my suspicion is that Lime are making the same cost-saving/risky approach that Mobike/Urbo/Ofo et al have done so – they don’t use have GPS on the bike itself, but are primarily using the GPS on your smartphone. In Lime’s case they may have a SIM card or emergency GPS for retrieving a missing bike – but not in regular operation. When I stopped at the bottom of the hill on Camden Road, I switched away from the Lime app (but had it open in the background) to the Beeline app, to activate my device’s functionality and start sending it GPS information. Unfortunately, it looks like this stopped the Lime app from recording my location – although the clock kept ticking. So, it looks like I only did a 2.5km journey, not the full 7km:

Journey of 2.5km according to Lime app – the “finish point” being where I paused to put on my speedometer and switched to another app in the foreground.Actual journey on the Lime bike – 7km.

This issue may be a Huawei/Android 6.0 thing – it could be because the Lime app doesn’t have permissions to access the GPS in the background – or Huawei’s battery “optimisation” cuts off its connection in the background anyway – this has already caused me problems – but it should have been clear to the app that if it wasn’t getting GPS information from my phone, it should be using the bike’s – so I don’t think the bike has any, or it’s not used.

I also didn’t switch back to my Lime app immediately on finishing the ride – I just drew the lock catch back and felt a buzz from the phone that was confirming the ride was finished – a couple of Lime notifications on my lockscreen also indicated that it had detected the journey finish. But – I only unlocked my phone and switched to the app once I had walked ~200m further into the UCL courtyard. The app has then marked the bike as being in the UCL courtyard, not where it actually is (which I am showing here as the green pin to the north):

Wrong location…

This might be quite tricky to someone trying to find the bike – they’d need to head out of UCL, along Gower Street, and then up Gower Place to find it. It looks like Lime again used my phone GPS as soon as it could – well after the ride finish – so has recorded the wrong location.

It may be that it will later use any SIM card on the bike to triangulate its location correctly (or even its GPS if it has it – I suspect not) and snap back to Gower Place. But, this kind of asset tracking trouble is a nightmare both for users (they can’t find the bike) and the operators (they can’t find it either!). This is one of the reasons Ofo essentially failed – they couldn’t find their own bikes but with the higher costs of electric bikes, I’m really suprised to see it again. In mitigation – there are very tall buildings here and the street is narrow – so it could be a simple GPS error too. Indeed, as well as the “lime symbol” (bike location) being wrong, the blue dot (my location) is also wrong – I’m standing at the “crosshairs” symbol on the map above when I took this screenshot.

(Update: As I suspected, the bike does have communication capabilities of its own – it has “phoned home” after an hour or so, and the location has updated to be much closer to its actual location)

So, to conclude, getting a Lime-E to work didn’t work out for me – it cost more than the tube, and took longer, and still required a lot of pedalling. However, I’m not the target user I suspect – it’s people who wouldn’t be cycling anyway, and just want an easy way to get around, not in a great rush, and maybe with a little bit of exercise but nothing too strenuous. I don’t think most parts of London have enough hills, to make the relatively high cost of Lime worth it here – although I would love to try it out on Swains Lane. Maybe a user-configurable app option could change the profile on the bike, to allow a decent boost between 20-25km/h.

I think electric bikeshare has a place in London. We aren’t quite there with Lime. They are doing a lot of things right – not overwhelming the streets, looking after their fleet fairly well (I never see them knocked over) and allowing sensible usage anywhere – but they are also making some of the mistakes which the older dockless companies (Ofo/Urbo/Mobike) also made in London. They are also, like almost all the other companies in the space here, not sharing their bike locations publicly/openly. You either have to open the specific app for the operator, or happen to see a bike when you weren’t expecting it (like me today). If Google Maps, Transit or CityMapper had told me of these, then surely they would be used more and more effectively. Get your GBFS feeds out there, bikeshare companies, regardless of if you are mandated to (big American cities) or not, and let people find your fleet in new and better ways!

I’m not quite convinced we have arrived at the future of smart Mobility as a Service (MAAS) just yet, at least in London, but at least there are various companies working on it. It’s going to be an interesting summer.

Two Lime escootershare scooters being used on the former highway in Paris beside the River Seine that is now a peaceful, traffic-free route. The scooters are passing a rather well hidden New Velib bikeshare docking station.

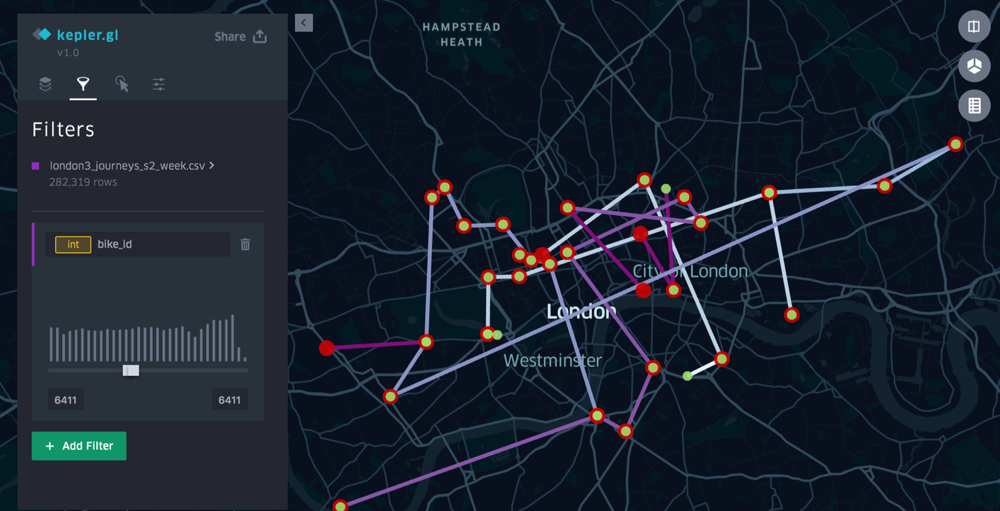

I was in Paris just before Christmas, taking part in a workshop at IFSSTAR (Université Paris-Est) on innovations in flow visualisation – GFlowiz. I talked/demonstrated some old and new ways that I and others have shown commute journeys in the UK on the web, looking both at The Great British Bike to Work and TubeCreature (developed with the HERE mapping platform), as well as some tests, with open bikeshare data, of the new React/WebGL/Deck.gl-based Kepler.gl recently developed by the Uber Engineering for interactively visualising large spatial datasets locally in a web browser. Kepler.gl works well with bikeshare flow datasets of up to around a million journeys, which, as CSVs with lat/lon pairs, can be simply downloaded, dragged and dropped into the web application:

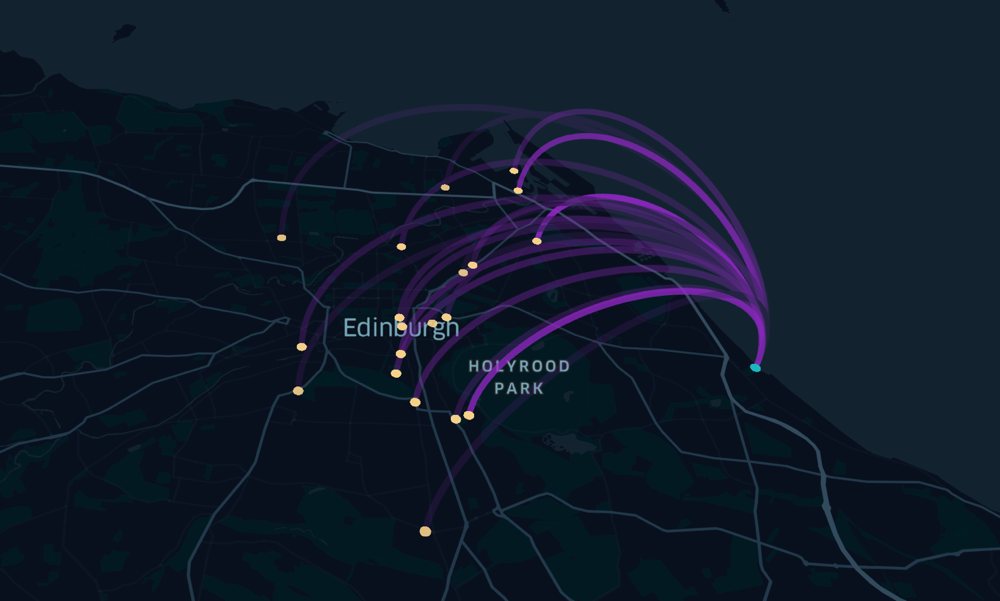

Showing the journey of a single Santander Cycles bikeshare bike over a week in July, using Kepler.gl. Journey starts/finishes are green/red and the lines become more purple as the week progresses.

I enjoyed the other talks in the workshop too, especially the introduction to flowmap.gl by its creator, Ilya Boyandin of Teralytics.

I had a few hours left after the conference to explore the centre of Paris, so I embarked on a long walk from Forum des Halles to Notre Dame, and then up to Gare du Nord. Paris has undergone a bit of a shared/smart mobility revolution on the quiet, since I last visited a couple of years back. Escootershare has taken advantage of the disastrous start to the relaunch of Velib at the beginning of 2018, and France’s more liberal traffic laws than in the UK, with numerous companies launching their operations there. Some dockless bikeshare systems have had a go, although Ofo at least has now disappeared from Paris, and the trend for the rest doesn’t look good either.

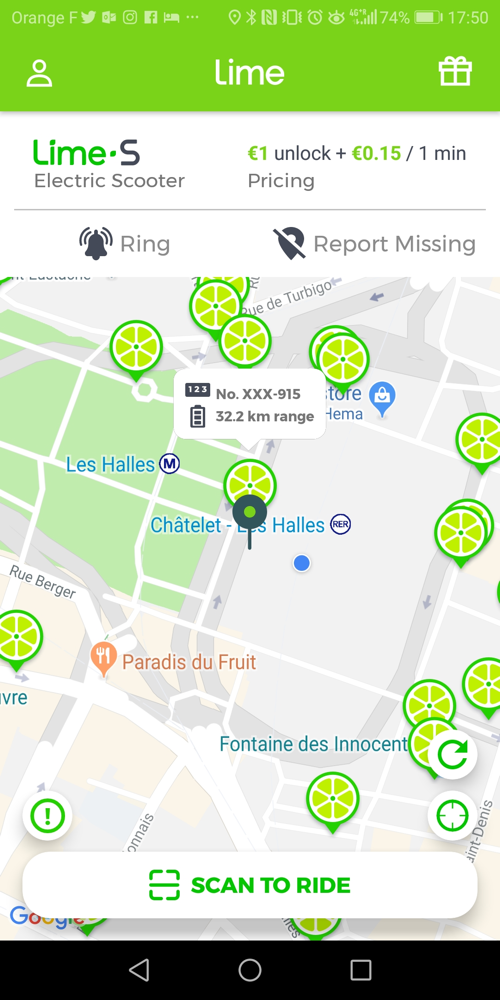

Lime escootershare bikes available (according to the app)

So, along my walk, I noted down all the escooter/bikeshare brands in use that I could see, along with the incumbent Velib service. There were also quite a few personally owned (or possibly white-label shares) that I spotted scooting past, which I didn’t note – for scooters at least, these were in total easily outnumbered by the brands.

Escootershares are, at the moment at least, all dockless, rather than being locked in physical stations, and I believe they tend to get taken in by casual workers overnight for recharging. My walk took place between around 6pm (i.e. end of rushhour) and 8:15pm, and I saw plenty being operated even at the end of the survey interval, so I would presume that the escooters are generally collected after this time.

Overall, I was impressed both by the uptake of these devices, and the care in which they were left after use. I saw no sign of any vandalism (although I did mostly stay in the more touristy parts of central Paris) and very few were inappropriately parked. I can’t say for sure that all the ones I marked as parked upright were not blocking pavements or crossing (e.g. tactile strips, dropped kerbs) in such a way that someone in a large wheelchair might have an issue, but on the whole I got the sense that they were not the pavement intrusions or litter that many of the London dockless bikeshares have become.

Five “Bolt” escootershare scooters – the only “group” of scooters I saw in Paris.

So in summary, from my unscientific survey, the dockless bikeshares are not really being used at all, the Limes and Birds are being well used, the new Velib is being used but not in the numbers I would have expected, and they are all generally being left tidily. I have no doubt that, in their current configuration/use level and street scene impact, the escootershares are a positive to the city. They are not cluttering the streets, and those that are there are being well used. There are too many operators, for sure, so some consolidation is needed – no one wants 6 share apps on their phone, but Lime and Bird at least have a good level of usage. It is very sad to see the Mobikes lying around unused, and with so few left, but they were a bike that was, initially at least, not properly designed for the European market. You can’t take shortcuts with new mobility solutions if you want them to actually be solutions. Maybe their lower profile approach will allow them to spot the markets where they can thrive, and give them the flexibility to adapt as necessary.

In London, we’ve moved on a bit from the autumn, where both Ofo and Mobike had retrenched considerably from June’s moment of “peak bikeshare”, even though we’re a long way behind Paris, thanks to escooters essentially being illegal both on pavements and public highways.

Mobike has expanded a little bit again, back to Ealing, although their two operating areas in London are very small. The bikes are generally now always in operator-placed groups, and while these are very visible, there are few bikes which are on their own, suggesting little use by actual genuine users. They’ve massively densified the number of bikes available in the areas, however they have attached “£20 fine for leaving bike out of zone” type stickers to all the bikes – and as these zones have changed several times since launch, I can’t blame users for not daring to use the bikes. I would not be surprised if they were seeing less than 1% of the journeys (or 10% of the j/b/d) of Santander Cycles. They also seem to struggle to monitor where their bikes actually are, or what state they are left in, as the few that are out of the operator-placed groups, are often left knocked down, for days at a time. It’s not a good look on London’s pavements, and it’s an effective way to lose the non-riding public’s sympathy unfortunately.

Ofo’s operating area didn’t shrink down as far, but unlike Mobike they haven’t restocked, so there are very few bikes to be seen anywhere in central London or the other parts of the operating area. It’s almost impossible to find one for a journey, now.

Both stolen Ofos and stolen Mobikes are appearing less often. This is probably because there are less available to steal, and the ones that were stolen are probably in very bad condition now. Occasionally you still see a youth on a stolen one, the bike sounding like it’s about to fall apart.

Lime has launched their ebikeshare in west London (Ealing, parts of which still have Mobike, and Brent, which was supposed to have had Mobike too but didn’t launch). You can’t officially therefore take Lime Bikes into central London. I don’t know if the motor cuts out if you do, but quite a few are appearing in central London anyway, and I think you may even be able to start from here (i.e. out-of-zone). Their starting price is very expensive though – £1 + 15p a minute. This means, after 3 minutes, it would have been cheaper taking the bus, tube or train. £1.50 flat rate for half an hour would have been better. But it’s a start, and though they are not escooters, unlike in Paris, the strength of the Paris operation suggests Lime knows something about how to run these.

There is also an escootershare in London! Bird have launched. However, it is only available on a single route in East London, on park land that is not covered by pavement/public road restrictions. You can scoot your “Bird” between Here East, the former London 2012 Olympic media centre which is now a start-up hub that is currently very poorly connected to tubes/trains, and Stratford station, which is incredibly well connected. Again, they are very expensive – £2.50 a ride. There is a free shuttle bus between the two points, too. So, really, it’s acting as a demonstrator. But, you have to start somewhere for escootershare in the UK and this is a start.

Santander Cycles are still not expanding, and unlikely to ever expand with TfL’s new financial woes and insistence on building very expensive permanent powered docking stations with card terminals, in a high density formation. But they did record five consecutive months this summer with over a million journeys each month. Their fleet seems to be in good working order and popular. I still think a redeployment of some docking stations further out, cheaper app-only stations, and an introduction of a Bike Angels style user rebalancing, would enhance things, but the system/contract is I suspect not set up to encourage radical innovations like this.

I look forward to 2019 as a year in which smart mobility technologies will continue to make cities better places. Look out on this blog for some exciting news, soon.

Journeys from/to a Just Eat Cycles docking station in early December, in the east of Edinburgh. Visualised in Kepler.gl. Translucency is being used to indicate multiple journeys between the same two stations.

I recently presented at the CoMoUK Good Mobility Conference in East London, looking at the story of bikeshare in London over the last 12 months ago, touching a little on other systems in the UK.

Here are my slides, slightly updated from the conference itself:

While the core of the presentation was a timeline, numbers and data from London’s bikeshare between last summer and this summer, I took the opportunity to also rate the various UK offerings on their open data provision, and offer some of my thoughts on round 2* of dockless bikeshare which took place this year.

It was great to hear a wide range of presentations at the conference. I particularly liked the Derby presentation. Thanks also to Tim, operator of Derby, for sorting out the GBFS feed. Thank you to CoMoUK for inviting me.

* Round 1 being oBike’s “forgiveness” model back in summer 2017, and round 3 being, I’m sure, American dockless providers “getting it right” next summer.

Having travelled to both Milan and Singapore in the last few weeks, it’s worth a note on the bikeshare provisions there.

Milan – BikeMi, Mobike, Ofo

Milan has BikeMi, a long-serving dock-based bikeshare system, which is one of the nearly 400 city systems that I have mapped in Bike Share map. It covers a big part of the city. There was a docking station close to both my hotel and to the location of the the conference I was attending, however far more noticeable were the numbers of Mobikes around the streets. Ofo also operates in Milan, although their bikes are not as prevalent.

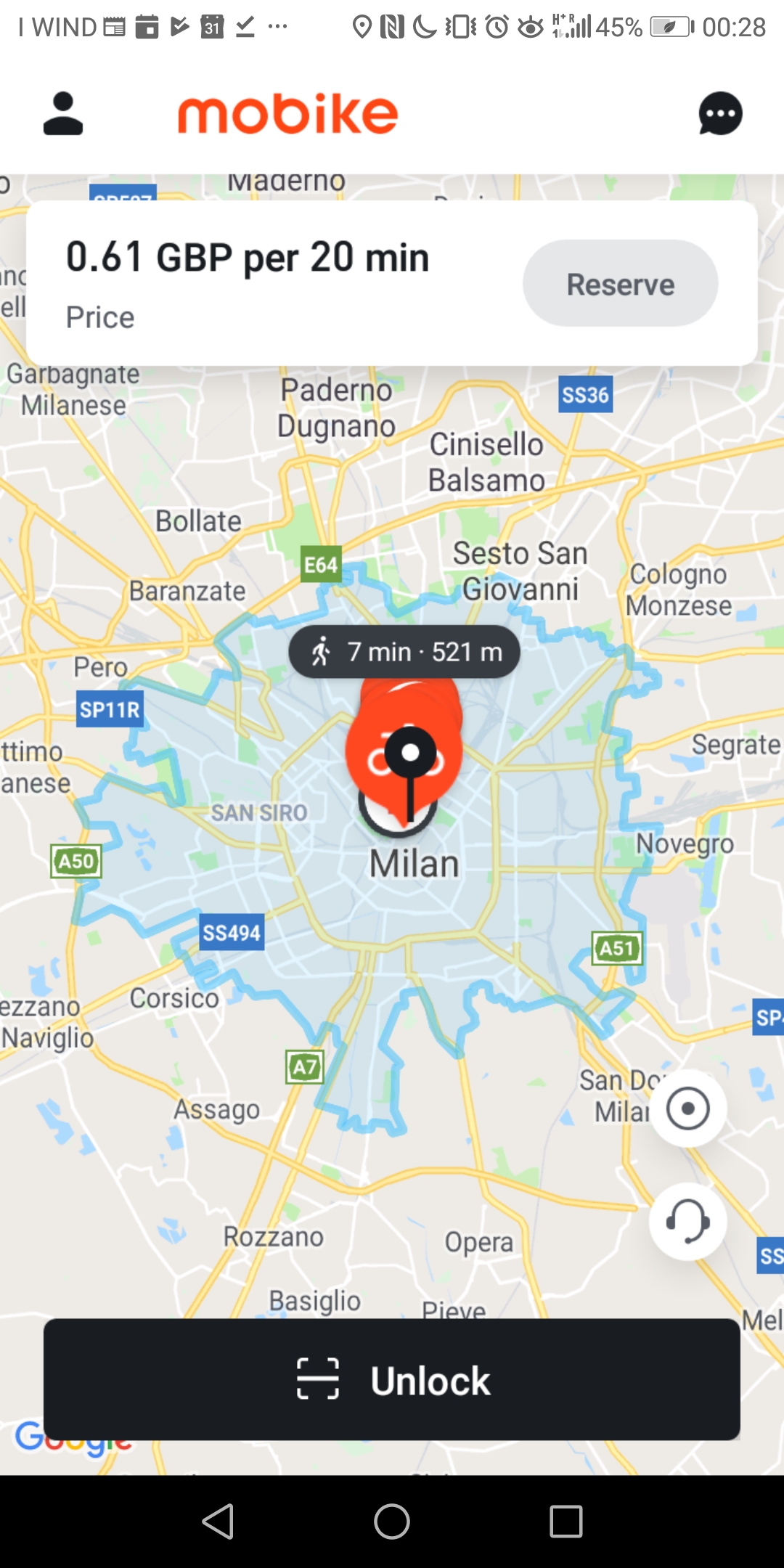

I ended up using Mobike – mainly because I already had the app installed on my smartphone, for my occasional usage in London – and Mobike, like Uber, works nearly seamlessly across the various cities it operates in. This simplicity, combined with the new EU free roaming laws meaning that I can use the app without incurring roaming data charges, and the fact there was one to hire just around the corner, means that Mobike for me won over BikeMi. It’s a problem that dock-based systems are going to struggle with, unless they can somehow collaborate with each other globally. Perhaps a start would be JCDecaux “Cyclocity” systems allowing use across their cities if you are already signed up for another one, and a similar approach for Motivate and Nextbike systems. Although, as each city typically has a monopoly dock-based operator, this approach still has a more limited approach.

(I say nearly seamlessly – both apps struggle a little initially when moving to a new city. In Mobike’s case, the system boundaries generally don’t appear until the app has been restarted a number of times, after moving to a new city. For Ofo, the pricing indication is initially wrong – I’m pretty sure it’s not free!

Mobike and Ofo have not suffered in Milan like their have in London. They both operate throughout the historic centre of the city, and much of the suburbs, rather than being artificially constrained on a borough-by-borough basis like in London, or only operating in small sections of the city by operator choice/resource limitations, like in Oxford and Cambridge.

Milan does not have as much in the way of dedicated cycling infrastructure as London, however I generally found a good level of respect from drivers and felt comfortable moving around the city. It was exceptionally hot when I was visiting (35°C) and although I noticed a few other cyclists and also bikeshare users, there weren’t huge nunbers in London. I noticed that most of the Mobikes were single ones which had been left by the previous user, rather than stacked by the operator, and also more than once they had been left in a position entirely blocking the pavement and meaning the pedestrians had to get onto the street to get past. This is a big problem in many cities where dockless operators run systems – how to get users to park responsibilty. The solution – a combination of user attitudes, rules and facilities, is one that does seem to have been solved for the next city I visited…

In Singapore, there is no dock-based system but a wide variety of dockless operators have bikes here – as well as Ofo and Mobike, there are the home-grown SGBike and GBikes (the latter based on the SharingOS system), and OBike (cobranded GrabCycle) – which started out in Singapore. Both GBikesand OBike have ceased in Singapore, presumably their apps no longer unlock their bikes – but they are both scattered everywhere – or rather, this being Singapore, they are neatly stacked up against trees and fences. Will anyone remove the bikes for companies that have ceased to be?

Singaporians being extremely considerate people, I didn’t notice any bikes blocking pavements, or indeed showing any sign of lock tampering or vandalism. A small number of bikes had damaged wheels. Again, I have both the Ofo and Mobike app on my smartphone, but with no free data, and no particular need to cycle, I didn’t hire any bikes this time.

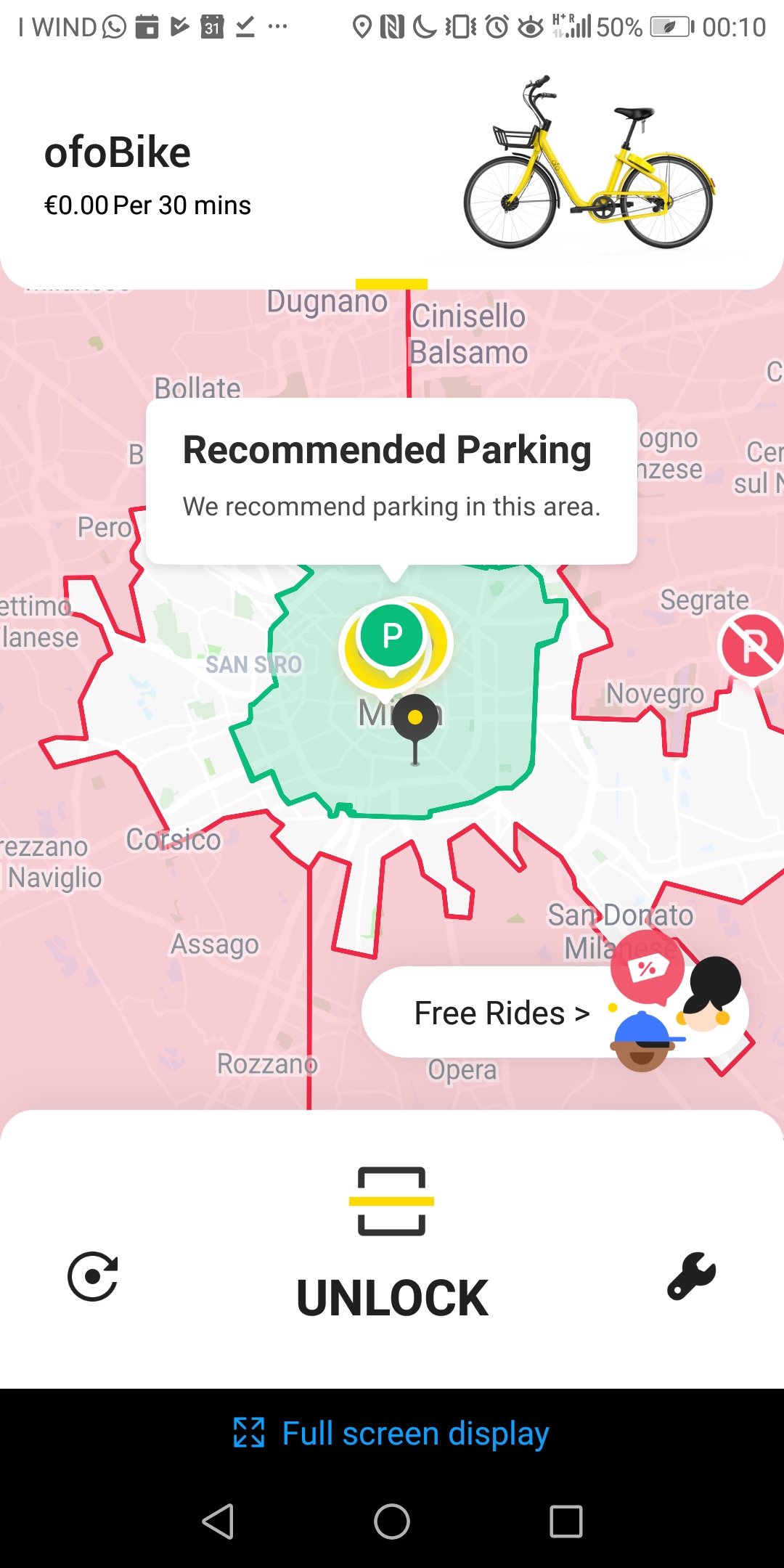

One thing I noticed over and over again is multiple operators bikes, being stacked neatly together. Sometimes, they were located within a painted rectangle indicating an “official” cross-operator permitted parking location:

Other times they were in “dead” pavement areas, such as traffic islands, where no one would otherwise need to be walking or driving:

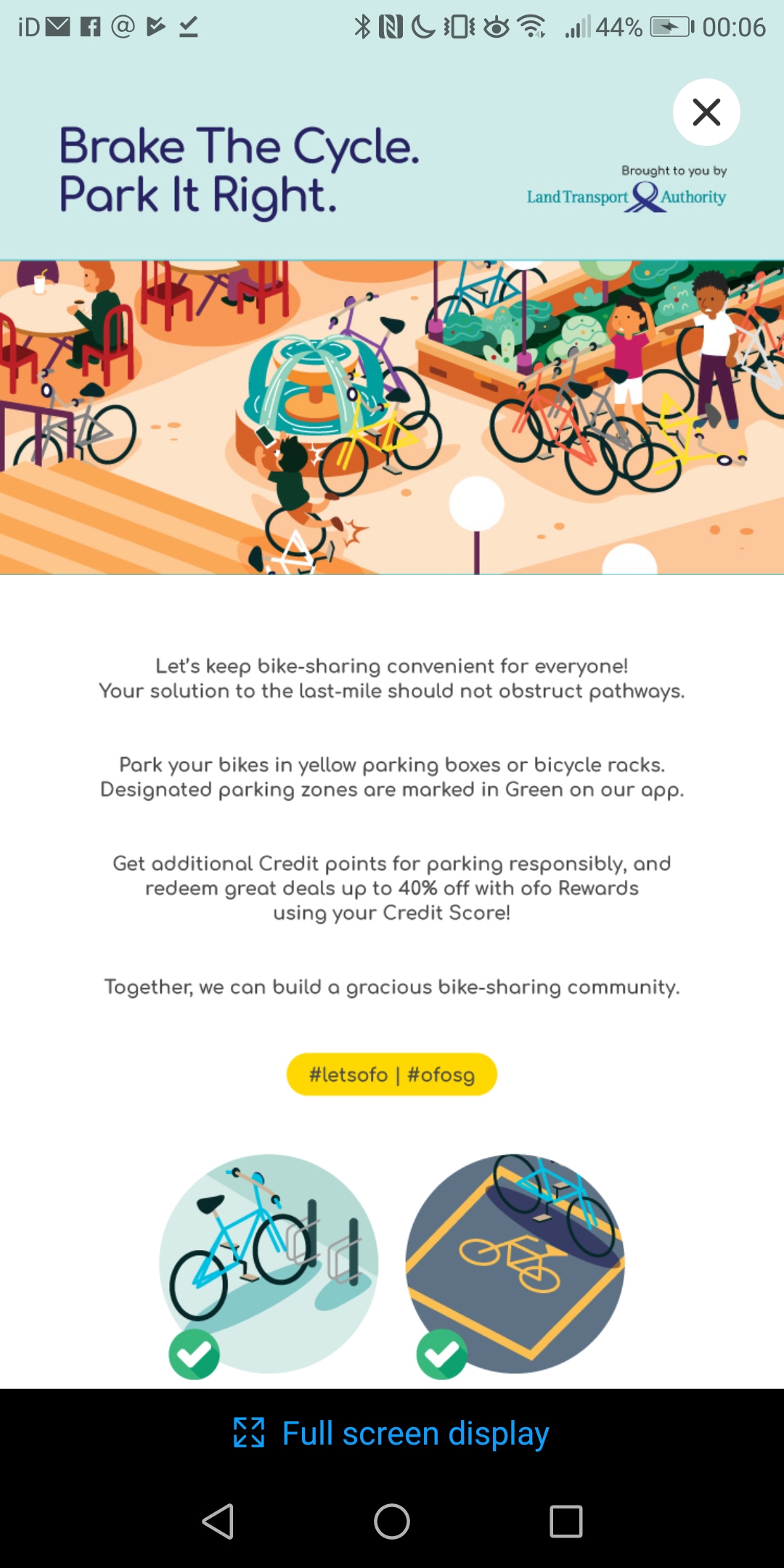

There is clearly some city council direct involvement with the operators – in Ofo’s app, there appears a message from the Land Transport Authority about parking neatly:

(Incidentally, GrabCycle is I believe a multi-operator marketplace/broker. I haven’t seen this before for bikeshare, and Ofo and Mobike are not currently part of it – they are presumably “too big” – but I think ultimately cities with multiple competitive bikeshare operators will likely have to eventually enforce/insist on allowing the bikes to be used through marketplaces. No one wants to have six bikeshare apps installed on their phone, and no city wants six incompatible bikeshare bikes sitting on every street corner, each only useable by a separate dedicated app.)

The central part of the city, at least, is not as bikeable (or walkable) as Milan – with large roads and the lack of much in the way of dedicated cycle lanes, the only cyclists generally seen were on riverside paths and in parks. Pedestrians also can come to junctions without any crossings – except perhaps by a nearby overpass. It’s all very well having a marked parking bay, but if it’s beside a huge road with no cycle lane, is anyone going to use it?

The high temperature (30°C) and humidity, characteristic of the city state throughout the year, doesn’t make it the greatest place for comfortable or leisure cycling. I saw almost no-one using the dockless bikeshare bikes, even through are are loads waiting to be used, but I did see plenty of people on eScooters – both for-hire ones and private ones. It is only a matter of time before these become huge in London.

Intriguingly, there may note be a dock-based bikeshare system in Singapore – but I did notice these bike docks. They are “semi-smart” docks – they have an electronic lock that just locks the front wheel, but they are small and unobtrusive, presumably much easier and cheaper to put in than London’s hard-wired, “street furniture” type docks. They were, here, being used as spaces to keep Ofos, rather than by the bikes they were designed for:

I did notice a number of interesting varients of both Mobikes and Ofos. They have been in the city longer than they have been in the UK, and so a greater number of models are on the streets – but as well as older versions, there are newer ones that have not made it yet to Europe. These newer ones generally look chunkier, with bigger locks.

Here’s a Mobike with a rather nice frame painting detail, an unusually chunky looking lock, and solar panels in the front basket:

Here’s an Ofo with a very chunky appearance, particularly the tires, which look like they could withstand anything. They are solid, but with lots of holes drilled through the rubber to presumably reduce weight and possibly generate a warning whistle (not really):

Notice also the SGBike and Mobike parked neatly beside by other users. Off the pavement, off the road, not knocked down. London, you have a lot to learn.

I did get the feeling that bikeshare might be a spent force in at least the central part of Singapore (I did not visit the suburbs) and eScooters may already have taken their place here. Coupled with Singapore not being a particularly cycling friendly city – certainly compared to London – I wonder if the only thing remaining is for the city council to sweep up the unused bikes for the bust operators, and tell the others ones it’s time to move on? I understand that the council has recently tightened up the regulations for bikeshare in the city, making it harder for the companies to operate, but a necessity in a city with the layout and streetscape like Singapore’s.

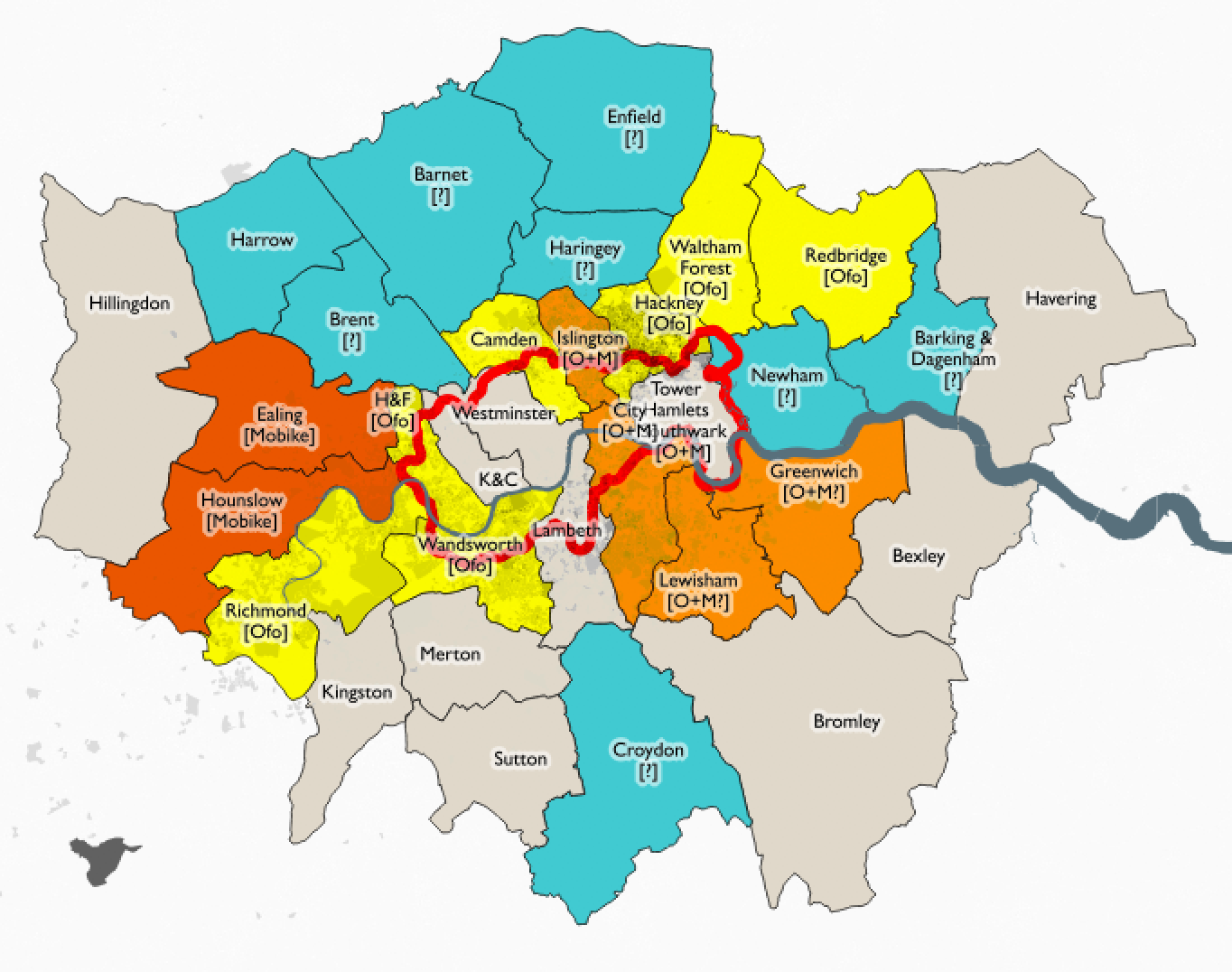

Dockless bikeshare has been out in London for around 10 months now (not withstanding the brief but spectacular oBike launch and burnout in mid 2016). It looks like the operators are getting serious and trying to get dockless bikeshare to pay for itself – starting a transition from a “growth” to “profit” focus:

Mobike has introduced an out-of-operating-area fee of £10 for London (left). Interestingly, this is only £5 for Oxford (right), where arguably the competition is even more fierce:

It isn’t clear whether you can continue to start journeys from outwith the operating area, but you must finish within them to avoid the fee. However, you can also get the fee waived by taking any Mobike from outside the operating area, back inside it, within 12 hours. It could be the bike you took outside, or another one. This is interesting – let the user help the system work better. You either fix the problem (bikes outside areas the operator can manage effectively, or don’t have permission to be in) or pay the operator to do it for you.

Mobike is making a bigger deal of its hubs now, showing the numbers of bikes currently available at them. Bikes in a circular buffer around each hub are reported as at the point in some cities (Oxford – left) but individually in others (London – right). This makes them a little more like a hybrid system, with certain locations generally having a reliable pool of bikes available, but with out-of-hub parking still available to keep the system flexible. At this point, there is no user incentive for hub-based journey finishes or starts.

Mobike have also shrunk their operating areas – in Islington, it now doesn’t extend north of Holloway. Presumably Mobike are tired of moving their bikes back up the hill to Archway and Highgate, only to have everyone cycle them back down. However they have extended into a small part of Hackney – the De Beauvoir Town area. They have also shrunk their Southwark footprint, so that the bikes can only be used north of the South Circular, and their western footprint has also shrunk – no service in west Hounslow, Feltham, Southall or Greenford now. They has also completely pulled out of Newham. Looking at their app, it never looked like there were many bikes available for use there anyway. You can see the area of operation here (orange border).

In addition they have significantly increased their usage fee. Initially it was 50p for 30 minutes. Now, it is 50p for 20 minutes on the smaller-frame bikes with black baskets (show as orange on their map), or £1 for 20 minutes on the larger-frame bikes with orange baskets (shown as white on their map). [Updated 12 July – now £1 for 20 minutes for all their bikes.] [Updated 1 August – now 99p/20 minutes.]

Ofo has also increased their usage fee, it is now 70p for 30 minutes. [Updated August – now £1 for 30 minutes.] So, in places where both systems operate, the small Mobikes are cheaper for journeys up to 20 minutes, the Ofos are cheaper for 20-30 minute journeys, the small Mobikes are cheaper for 30-40 minute journeys etc etc…

Single Journey

Ofo

Mobike Small

Mobike Big

Santander Cycles

15 min

70p

50p

£1

£2

25 min

70p

£1

£2

£2

35 min

£1.40

£1

£2

£4

45 min

£1.40

£1.50

£3

£4

1h 15m

£2.10

£2

£4

£6

1h 45m

£2.80

£3

£6

£8

Subsequent Journeys in next 24h

Ofo

Mobike Small

Mobike Big

Santander Cycles

15 min

70p

50p

£1

Free

25 min

70p

£1

£2

Free

35 min

£1.40

£1

£2

£2

45 min

£1.40

£1.50

£3

£2

1h 15m

£2.10

£2

£4

£4

1h 45m

£2.80

£3

£6

£6

Ofo and Mobike are also now showing specific forbidden areas on their app. This is interesting, because I assumed that all areas outside of their operating area were forbidden. Presumably these are extra-problematic areas for the operators. Ofo has marked various royal parks as forbidden areas, while Mobike has marked canal-sides, the London Bridge station complex, and large public parks, as forbidden. Mobike’s out-of-operating-area areas allow journeys to finish but the user (only) is then encouraged to move the bike back into an operating area within 12 hours, it is locked out of use for others.

This means that in effect there are five types of dockless system geofences, with four being shown on the maps in the Mobike and Ofo apps:

Ofo

Mobike

Hub area

Shown in app as points overlaid on green-bordered rectangles. Parking here encouraged, occasionally incentivised with free next ride coupons.

Shown as points, but a blue circular buffer is shown on clicking it. Parking here encouraged but not incentivised.

Operating area

Show as green-bordered areas

Shown as blue shaded/bordered areas

Out of operating area

Shown as regular map. Parking locks bike for user-only redistribution back.

Shown as regular map. Parking results in fine, unless it (or another) is taken back in in 12 hours by the user, but still available for use.

Forbidden area

Shown as red shaded/bordered areas. Parking may result in credit drop or penalty.

Shown as grey shaded/bordered areas. Parking may result in credit drop or penalty.

Out of region

Not shown by either. But I assume there is a distance, out of the operating area, beyond which the operator would not seek to recover the bike into the operating area, but might sanction the user instead. For London, the GLA boundary might act as such an area

Meanwhile, the third dockless player in London, Urbo, has announced it is quitting the three London boroughs it is operating in – Enfield, Waltham Forest and Redbridge. Enfield will announce a replacement “soon”, Waltham Forest is getting Ofo in instead, and Redbridge already has Ofo. The numbers don’t sound great – only 6000 journeys in Waltham Forest in 5 months, on a fleet of 250 – so 20 journeys a day, or 0.16 journeys/bike/day, and 3000 miles clocked up in Enfield, again in 5 months, on a fleet of 100 – so (assuming average journey of 1 mile) 0.2 journeys/bike/day. This means these bikes are spending 99.8% of their time not being used (assuming an average journey of 15 minutes).

Barnet had just announced that Urbo was coming there, and Barking & Dagenham was due to sign-off Urbo coming there in July – I would speculate that these launches may be off. Urbo, an Irish company from the start, has just been bought by the operator of several bikeshare systems in towns in Ireland, and it has just launched Dublin, where it has access to the whole of the city. Just like in London, Dubliners likely want to cycle throughout the urban area and not within arbitrary political boundaries. So that would likely be where the London Urbo bikes are going.

Numbers of bikes and journeys are generally hard to come by for dockless bikeshare – the companies themselves have good commercial reasons for being coy with the numbers. In some cases, the operator will have fewer bikes out on the streets than they say – as they just don’t have that many (working) bikes – Santander Cycles have consistently overstated the numbers of bikes out there . The opposite can also be true – where dockless operators have agreed maximum numbers of bikes with boroughs, and then see these numbers be exceeded as users cycle over from neighbouring boroughs, or operations necessitate. There is little data, so we generally have to go on press releases:

Number of Ofos, Mobikes and Urbos in London

I am adjusting the following table as I get better information:

In better news, both Ofo and Mobike are both continuing to expand in London this summer, in areas where they do think dockless bikeshare will work. Mobike should be coming to Haringey soon, while Ofo have today announced their forthcoming expansions – Camden launches this week, with Waltham Forest following shortly (this week, says the borough at least), followed by Wandsworth and Hammersmith & Fulham. This means yellow bikes will soon be appearing in Bloomsbury, Fizrovia, Camden Town, Kentish Town, Highgate, Belsize Park, West Hampstead, Walthamstow, Chingford, Leyton, White City, Hammersmith, Fulham, Putney, Wandsworth, Battersea, Balham, west Clapham and Earlsfield.

There’s lots of bikeshare systems in the UK now. As well as the third generation dock-based bikeshare systems, fourth generation dockless (and hybrid) systems are starting to appear on various streets around the country, led by Mobike, Ofo and Urbo, three dockless providers and operators.

I’ve put together this simple model to try and understand where systems are most likely to be successful, for which I’m defining as a lot of (legal) journeys made with each bike placed by the operator. To do this, I split the country into its local authorities, apply three scores, and then multiply them together to produce an overall “propensity for bikeshare”, or PFB score (the name is a nod to PCT.bike from Lovelace et al) which can then be ranked.

Many mid-sized cities in the UK have their own local authority, approximately covering the urban area, while Manchester and London are split into multiple LAs. Conversely, some LAs individually cover multiple smaller towns/cities and large rural areas too. Hence, this is a very simply model which is not going to be completely fair to every urban area (Stirling, in particular, gets pushed well down the rankings as its LA includes a huge rural area). Still, for most of Great Britain, it produces results I would anticipate and is a good start towards potentially developing a more sophisticated model. The local authority geography is also appropriate, as local authorities act as the gatekeepers for which access is negotiated (for systems which pay themselves) or as authors of bids for subsidised systems.

Model Inputs

For this first, simple model, my three compounding factors are:

Residential and workplace population density – on the assumption that bikeshare systems need a critical mass of people passing by their bikes/hubs/docks, in order to be seen and used sufficiently frequently to justify the costs of equipment/maintenance, on the basis that a major source of income is per-use fees. Both residential and workplaces populations are used, as people have journey opportunities that can be facilited with bikeshare, both from their office (e.g. lunchtime errands, commute to evening socialising or back home) as well as their home location.

Proportion of people who already commute by bicycle, again looking at both workplace location and residential location (bearing in mind that many commute journeys, particularly in London, cross local authority boundaries). While such people are less likely to convert to bikeshare, as they already have a means of cycling, their presence on the streets and associated culture and facilities (e.g. bike coffee shops, marked cycle routes or existing cycle-friendly infrastructure) help normalise the idea that cycling is a possible option for a journey need.

Vandalism rate – theft and criminal damage to bikeshare bikes happens and it is an expensive one for the operators. It can be what causes systems to fail – particularly if they run out of bikes, or broken bikes litter the landscape and turn public opinion against the concept. While the dock-based systems are less vulnerable to this, as the bike is either securely locked to a clamp or in the hands of a paying user, dockless bikes are particularly vulnerable to vandalism, as they are not secured to immoveable objects, and their locks are, unfortunately, relatively easy to break by a determined offender looking for a free bike. The tendencies for vandalism of property that is not yours does vary significantly around Great Britain, while stereotypically it is likely to be more urban areas and areas with a younger and less educated population that is more likely to vandalise, using actual crime data on vandalism allows a more nuanced approach to be taken. Other crime classes (e.g. theft) were also considered for this model, but I think that vandalism rates act as a good proxy for how the local population around a bikeshare system will “care” for it or abuse it.

I have not included the absolute populations of local authorities in the calculation, as in general, with one exception (Isle of Scilly), LAs all have a significant night and/or day population, so they are all large enough to have a self-contained system. Another obvious factor, hilliness, is likely already correlated with proportion of cycling commuters and so is not included. N.I. is excluded from the model for now. Data sources include the latest police crime statistics (with populated-weighted averaging when across multiple LAs), and census data.

Results: Propensity for Bikeshare by Local Authority

Here are the results of the model run. Clicking an underlined title takes you to the main bikeshare for that area – forthcoming systems in brackets.

Some notes:

London boroughs score consistently highly, and even London as a whole, which is interesting as outer London is anecdotally not known as a particularly cycling-friendly place. Considering the size of the city, and the intimidating conditions cyclists often have to put up with in much of the capital, it is great to see it scoring so highly here.

Bikeshare operators are doing their homework and generally, the top end of the list is already well populated with bikeshare systems, in some cases multiple systems are competing.

The top local authorities without a bikeshare system (operating, announced or consulting) are Haringey, a north-London inner-city borough which has been surprisingly quiet until now, and Merton, an affluent outer London borough to the south. Oustide of London, the highest ranking areas without a bikeshare are Portsmouth (small system launching this summer), Gosport (neighbouring), Gloucester, Poole, Worcester and Hull. With the exception of Hull, these are all southern English urban areas, with generally affluent populations and some established cycling culture.

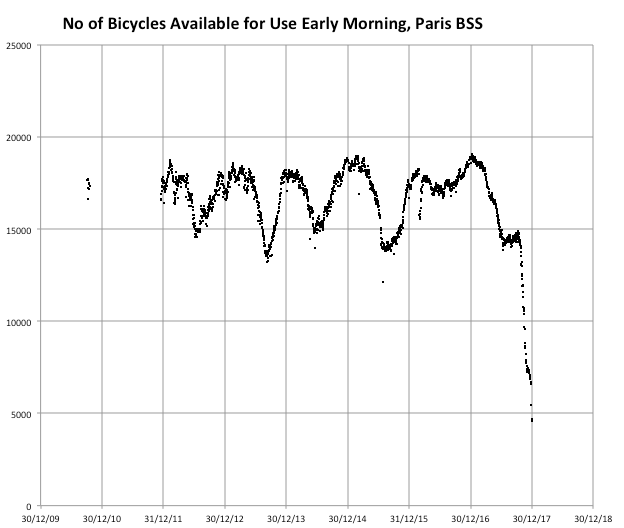

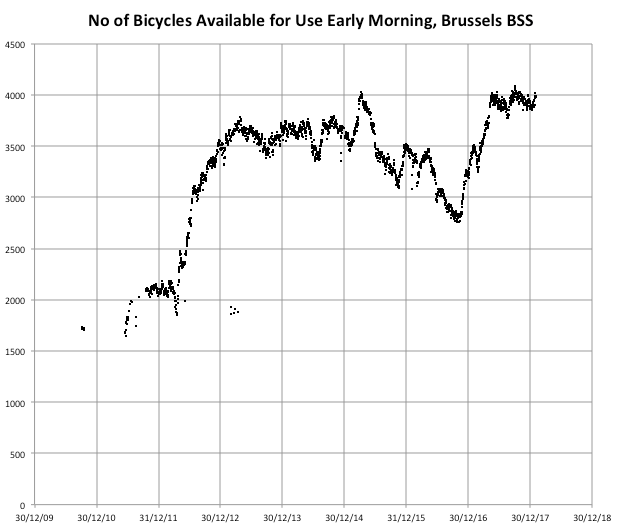

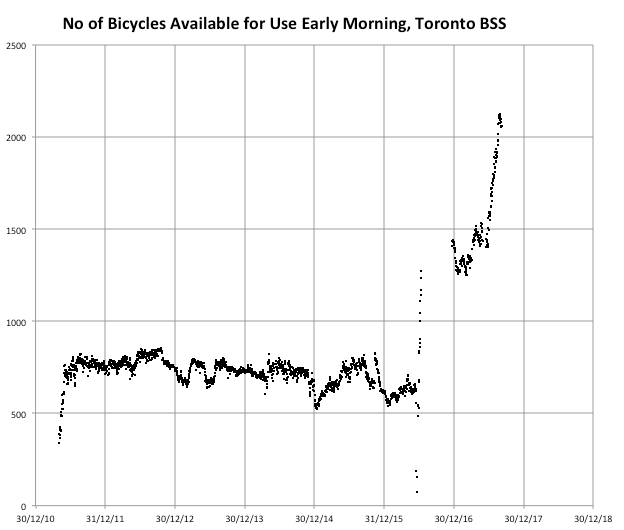

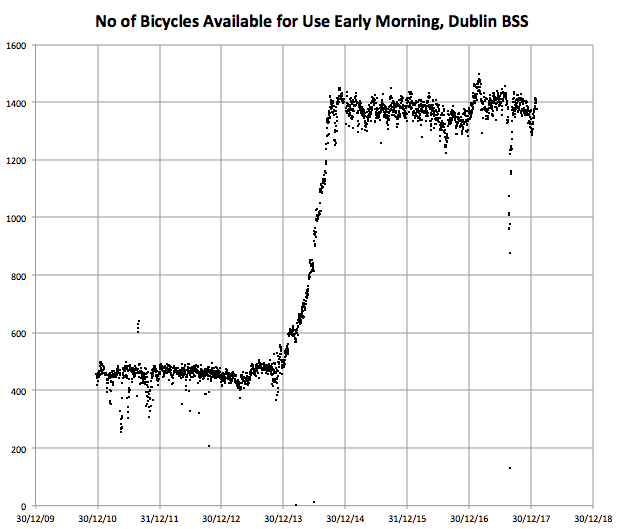

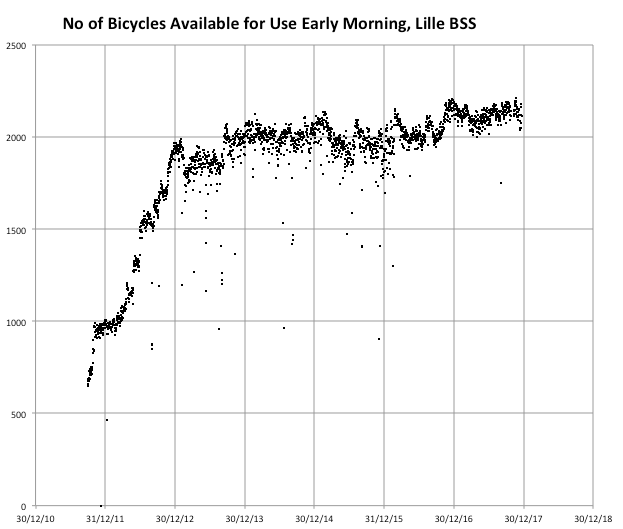

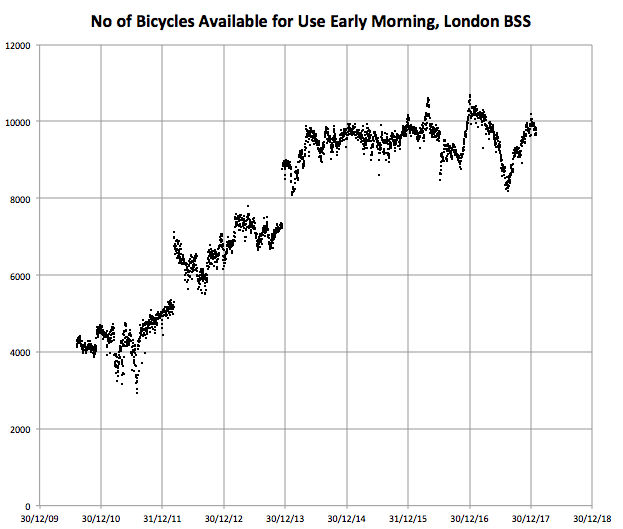

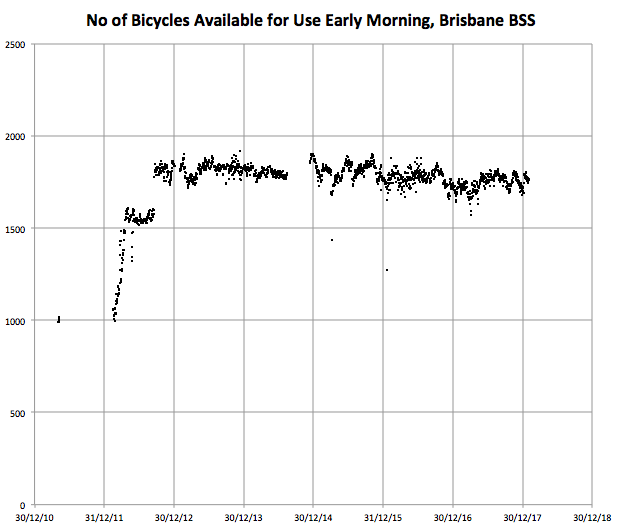

My research lab, the Consumer Data Research Centre, is making available much of the docking station empty/full observation data that I have been collecting, at frequent intervals (up to every 2 minutes) for generally the last 5 to 8 years, for over 50 cities around the world, to facilitate and encourage further quantitative research in the field. I already get numerous requests for this data – it is very interesting for all kinds of research projects, particularly because of it spans multiple years, so introducing this new mechanism is a good way to manage these requests. You can see the cities listed at the CDRC Data product page.

For three cities (Cork, Limerick and Galway in Ireland) we have directly attached the data to the record page. It is the data that has been collected up to the point that the record was published a few days ago, and on request we will reload the data, capturing more recent observations.

For the other cities, the data record is “Safeguarded”. This is because the logistics and technical limitations of attaching the very large amount of data to the records. Namely, it takes quite a lot of time to prepare each dataset for download, and the platform we are using is not designed for hosting extremely large files – plus, it is likely that researchers would want the most up-to-date data, meaning that we would need to build a mechanism to update the record regularly. Using an application process also minimises spurious requests – we have invested time both in collecting the data and processing it, so we need to be confident that it will be used. Additionally, some systems (particularly those in the USA) come with their own data licence restrictions from the operating companies meaning that we cannot freely distribute the “raw” data. In Europe, most of the datasets are explicitly open, meaning use of the data is unrestricted (although normally requiring attribution). the Irish cities listed above have a slightly more restrictive licence, requiring us to distribute it on the same terms, which we have done.

The data is available on application to interested institutional researchers. In practice, this means academic, public sector and non-profit organisations who which to carry out public/publishable research with the data. Application details are attached to each record.

Above and below are simple graphs produced from the data for various cities. I have looked at the number of bikes available every day at around midnight and plotted it on a simple graph against time.

Stay tuned because I am planning on releasing two further “data portals” of bikeshare data, soon. These are slightly more manageable in terms of file size and administration, so I am aiming for these to be directly downloadable.

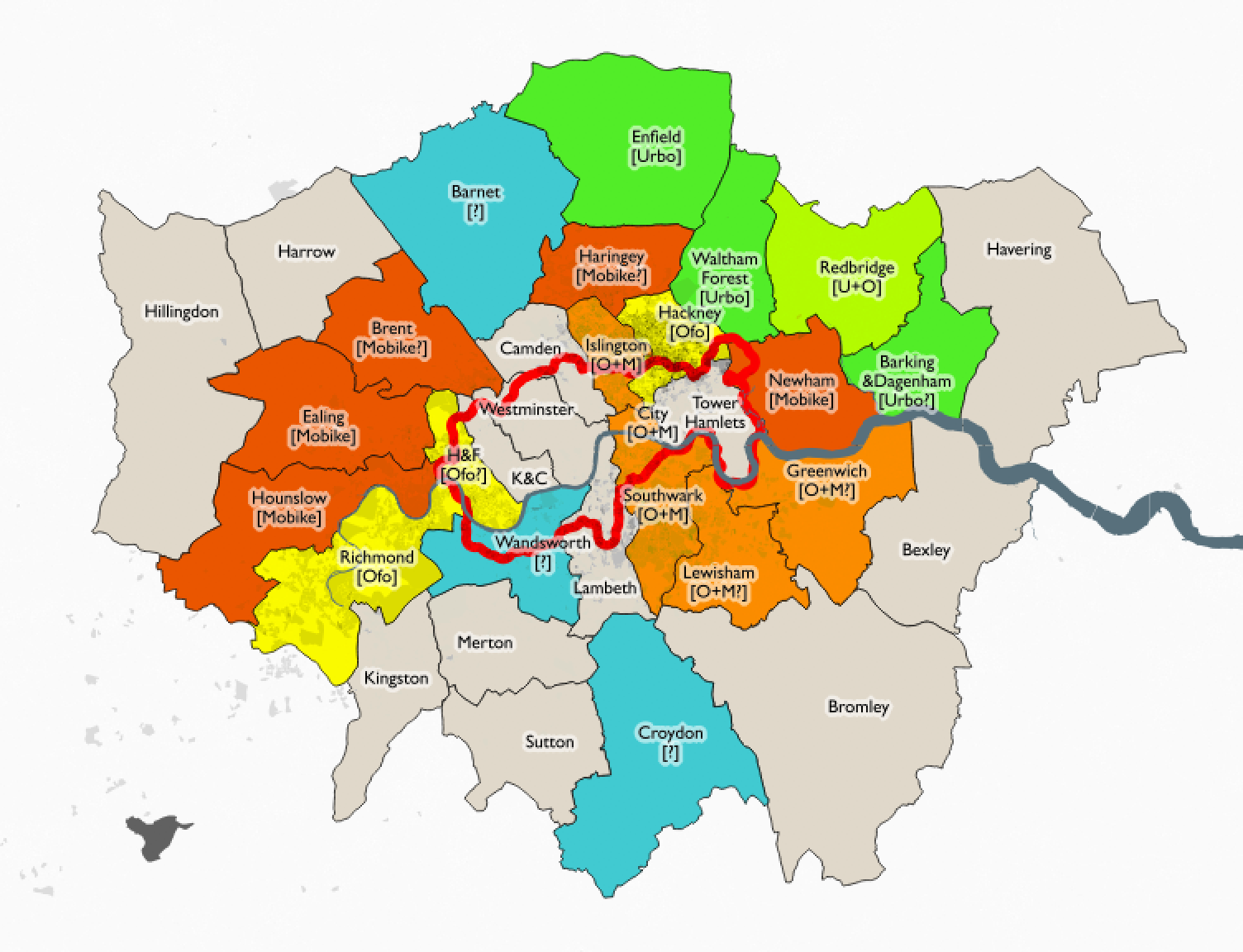

Mobike, one of London’s four bikeshare operators (with Urbo, Ofo and Santander Cycles) as today expanded to Newham. The operators are being driven by different borough approaches and priorities, which is resulting in a patchwork quilt of operating areas, although the London Assembly is today pushing for a more London-wide approach to regulation of the field.

Over and above the map linked above, I’ve done some population analysis to look at how the four different operators compare in London. Demographic figures are from the 2011 Census so total population will have gone up a bit, and cycle-to-work population up a lot. Nonetheless, the figures still allow for a useful comparison. The populations here are working age (16-74) populations. The differences across the operators are dramatic:

Operator

# of Boroughs

Area /km2

# of Bikes

Average Day/Night Pop

Bikeshare Bikes per Person

Pop Density pax/km2

Cycle To Work Pop %

Santander Cycles

5, + 6 (part)

112

10200

1,520,000

1:150

13500

4.8%

Mobike

6

196

1800

1,425,000

1:800

7300

3.5%

Ofo

5

123

1300

1,040,000

1:1000

8500

4.0%

Urbo

3

177

500

570,000

1:2800

3200

1.2%

I have calculated the populations by averaging the day-time workplace population and the night-time residential population, making a very rough assumption that people spend their waking hours split roughly between work and home. Santander Cycles, the dock-based system, has been around since 2010. The others are all dockless operators and launched in 2017.

The high population density where Santander Cycles works in its favour, as does its high bikes/population ratio, with one bike available for every 150 person who lives and/or works in the area. Urbo, on the other hand, is mainly targetting populations that both have a low population density, and a low cycle-to-work percentage – two factors that would work against it. Mobike and Ofo sit in the middle, with the former quite a bit larger than the latter at the moment, but the latter operating areas with a more established tradition of cycling (using here the Cycle to Work population as a proxy for cycling in general).

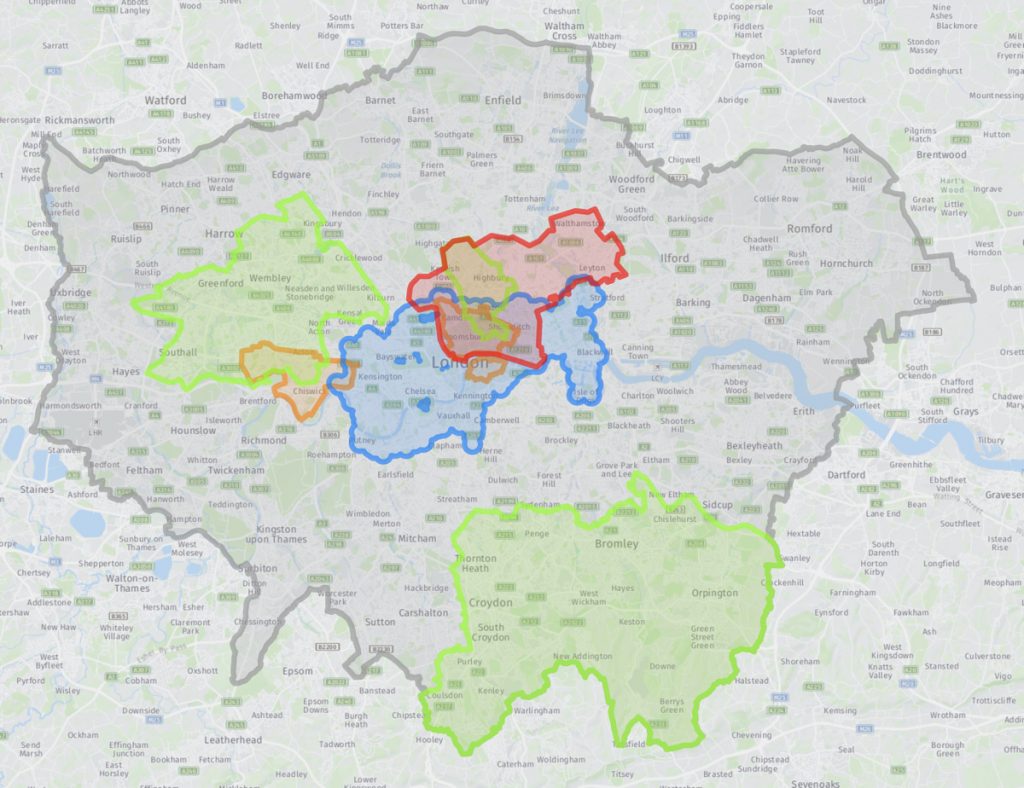

While TfL ponders London-wide regulation and freezes Santander Cycles, borough-by-borough rollout (and sometimes rollback) of dockless in London continues. I’ve rated each borough based on its provision – current, announced and rumoured (so likely some errors) of this all-important last-mile mobility addition to our streets:

Key

A – 2+ operators in/confirmed, at least 1 of which covers/allows >75% of borough and the other covers/allows >25% of borough

B – At least one operator, in/confirmed, covering significant part (>25%) of borough.

C – Operator(s) only covering small area, and/or only rumours of new operator.

D – No operators or positive news.

+ – Improvement expected soon.

* – Simple projected % for 2018, based on Census data – 2011% and 2001-2011 rates of change

I intend to keep this table up to date as things change, and make corrections where I discover things are wrong above. In case it doesn’t view correctly for you, you can see the full table on Google Sheets here. You can also see operator open data scores – check the tab at the bottom of the sheet. Nobody gets an A on this measure, though (GBFS+journeys).